The banking industry is increasingly focused on digital transformation with a foundation of data, applied analytics and artificial intelligence (AI). Banks and credit unions are leveraging AI to enhance existing offerings, create new products and services, and improve customer experiences. The application of data and applied analytics are also supporting the modernization of business models and decision making.

This transformation is not without challenges, including access to data, the quality of data, the availability of skilled talent and the deployment of resources for improved results. Most leadership teams at financial institutions also lack the digital and technological experience required to build a digital organization. Despite these hurdles, the decision-making capabilities, powered by data and applied analytics, can give banks and credit unions a competitive edge by generating significant incremental value for customers and the organization.

According to research from McKinsey, financial institutions that use data and advanced analytics to create real-time opportunities to engage with prospects and customers can increase value in four ways:

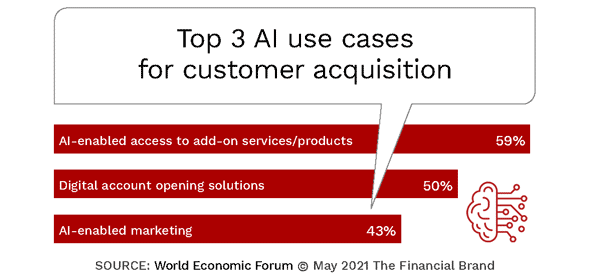

- Improved customer acquisition. By creating highly personalized messages at each step of the customer-acquisition journey, engagement is simplified and customer experiences are improved.

- Higher customer lifetime value. Cross-sell and up-sell of products and services are achieved through intelligent communication and contextual recommendations done based on real-time behavior analysis.

- Lower operating costs. By automating and simplifying data input, document processing, and decision making in both acquisition and servicing, efficiencies are achieved and costs are lowered.

- Lower risk. Using advanced analytics, screening of prospective customers and analysis of existing customer behaviors can signal potential risk of default and fraud.

Read More: The Future of Customer Experience in Banking is Personalized

The Opportunities for Using AI are Open for All

Building AI capabilities to maximize the use of data in the financial services industry used to be expensive, with limited use cases (e.g., risk and fraud analysis and trading). Recently, as with many advanced technologies, it has been found that cost barriers are falling, and that the ability to partner with capable solution providers has made it easier to deploy AI technologies. This is important, since more data than ever is being generated and since advanced decisioning capabilities are required to understand and respond to the fast-evolving needs of consumers with precision, speed and efficiency.

Financial institutions are increasingly looking to advanced analytic solutions to improve competitive positioning and enhance outdated business models. It has also been found that AI algorithms provide a ‘flywheel’ effect that rewards early movers – with economies of scale created when an accurate model attracts new users and additional data that increases the model’s accuracy. This is why advanced analytics and AI are moving beyond hype to gain more mainstream acceptance.

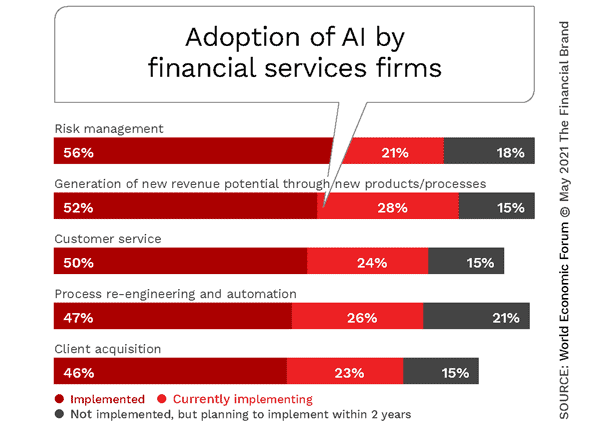

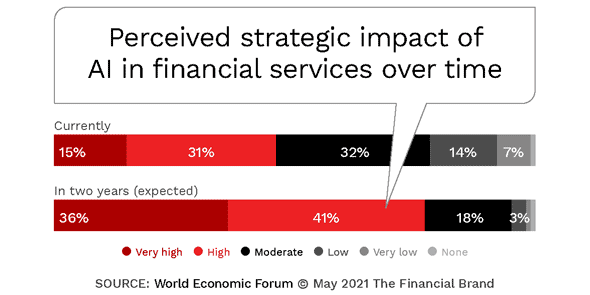

According to a study by the Cambridge Center for Alternative Finance and the World Economic Forum, a majority of global financial services firms have either implemented, or are currently working to implement, AI solutions across a wide variety of business functions. This study also found that the perceived strategic impact of AI is expected to increase significantly over the next two years.

Wake-Up Call:

85% of all financial institutions have implemented AI in some capacity, with fintech firms leading legacy banks and credit unions by a slight margin (90% vs. 80%) – World Economic Forum

Beyond initial risk and fraud use cases, an increasing number of financial institutions are using advanced analytics to create new products and services and a reimagined customer experience, positioning banks and credit unions as a trusted adviser at key financial decision moments. By automating advice and recommendations based on behavior and contextual opportunities, organizations can set the foundation for ‘self-driving finance’ which can ultimately position a financial institution as the primary financial provider in an increasingly competitive banking ecosystem.

Building Personalized Experiences Across the Customer Journey

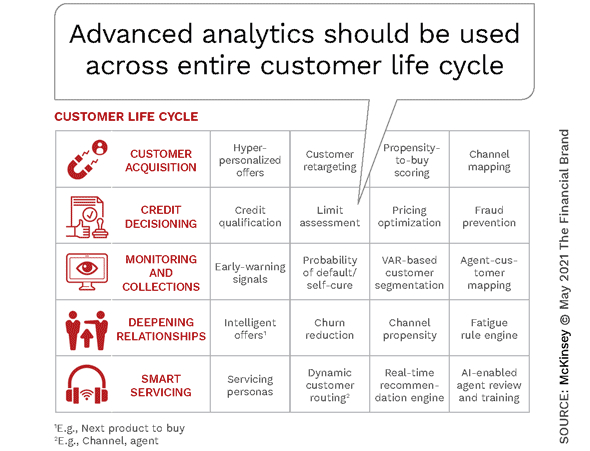

Advanced analytics should be used across the entire customer journey, from before the customer first engages with a specific financial institution, through the evaluation process, relationship deepening, ongoing engagement and even the servicing of the customer. The role data and advanced analytics play is center stage because few consumers or small businesses will follow the exact same path for the same reasons.

The channels used to open an account or manage a relationship differs based on the habits of the customer and the environmental factors that impact financial needs. The needs of the customer also change based on factors outside the financial institution.

AI Drives Efficiency:

Replacing much of the mass messaging that used to flow to thousands or tens of thousands of customers in a sub-segment, advanced analytics can help prioritize customers for continued engagement.

As an organization uses analytical tools to understand each new customer’s path to the bank or credit union and the path after a consumer opens an account, the financial institution will see constantly updated views of the customer’s context and direction of movement, which enables the institution to deliver highly personalized offers directly to the customer – in real-time.

According to McKinsey, “A financial institution can select customers according to their responsiveness to prior messaging – also known as their ‘propensity to buy’ — and can identify the best channel for each type of message, according to the time of day. And for the ‘last mile’ of the customer journey, AI-first institutions are using advanced analytics to generate intelligent, highly relevant messages, and to provide smart servicing via assisted channels to create a superior experience.”

The ability to increase engagement is the foundation for a strong digital relationship and ongoing loyalty. Organizations that are leaders in data use and advanced analytics use these tools to identify less engaged customers at risk of attrition and to create communication that will increase engagement … based on a customer’s unique needs and expectations.

Read More: Beyond Personalization – 3 Reasons to Focus on Customer Journeys

The Power of Deployed Analytics at Scale

To maximize the impact of data and advanced analytics, banks and credit unions should provide access to the insights created from AI technologies across the entire organization. This not only can result in improved decision making in near real time, but also support product development, product enhancement, personalized engagement and vastly improved customer service.

The key is to build a data strategy that collects 360-degree data insights from all touchpoints and deploys contextual recommendations that can be communicated to customers through multiple channels. According to McKinsey, “Leaders must encourage all stakeholders to break out of siloed mindsets and think broadly about how models can be designed for uses in diverse contexts across the enterprise.”

Marketing Opportunity:

While each customer-service journey presents an opportunity to deepen the relationship with the help of next-product-to-buy recommendations, banks should constantly seek to improve their recommendation engines and messaging campaigns.

The Importance of the ‘Last Mile’

Using data to create insights that can be used across the organization is not enough. Financial institutions must go the ‘last mile’ to make sure that accounts are opened, engagement increases, relationships are expanded, experiences are enhanced and loyalty is created. In other words, the return on the investment in data and AI is not maximized until the customer takes the desired action – on their terms.

Done effectively, the digital marketing engine can seamlessly integrate the data and insights created into highly personalized targeting and messaging that will deliver the right message, to the right audience, using the right channels … instantaneously.

The last mile also includes leveraging tools for continual testing and learning. The measurement process will identify components of content or distribution to improve, providing the ability to evaluate the effectiveness of initiatives in real-time.