While big banks have typically used technology and scale to crush smaller competitors, the underdogs are starting to make a comeback.

In fact, one report now says some smaller banks are adopting technology at a higher rate than big institutions, and they’re using it to find new competitive advantages.

But there’s a catch. So far only a handful of institutions are following this path out of the many thousands of traditional community and regional banking providers. Still, it confirms the competitive potential existing in many smaller institutions.

Kroll Bond Rating Agency (KBRA) looked at a group of what it calls “neo/hybrid” banks and found many are having success by rapidly integrating technology with their traditional operations.

Turning Point:

This new hybrid model can help smaller institutions turn the tables and leverage both technology and relationships to regain some of the market share they’ve lost.

A ‘Paradigm Shift’ in Technology Adoption

KBRA studied a group of financial institutions it calls the “KBRA Neo/Hybrid Bank Group” to see how they approached the use of technology within the areas of lending, deposits and processing. These institutions were notable for the differentiation in how they approached technology compared to their peers. Among the group were The Bancorp Bank, Cross River Bank, MetaBank and Axos Bank.

In recent years, consolidation in the banking industry has only increased the competition between megabanks with scale and smaller institutions that lack it. While fintechs and big players roll out shiny apps and new digital initiatives, smaller institutions have often found technology to be a complex and expensive hurdle to climb, according to the FDIC Community Banking Study.

However, since the start of the pandemic, there has been a significant paradigm shift in technology and investment rates from larger to smaller banks, KRBA notes. More community and midsize institutions are now finally taking greater advantage of lower-cost digital platforms to breach previous scale limitations and gain new efficiencies. One primary trend KBRA found is that smaller banks are taking a closer look at lower-cost platforms to redefine product delivery.

It’s a long-overdue move for many, but these financial institutions now realize they can no longer drag their feet on digitization. While the growth of remote capture, online account opening, and younger consumer behaviors have lessened the need for branches, the trend has only increased since the pandemic. As a result, the pace of branch consolidation has also accelerated. The lockdowns early in the pandemic forced even slow adopters to digital channels, and there’s a large consensus that many of these new patterns will remain.

While big banks benefited the most from this trend, the forced digitization has led other institutions to leap forward years in only a matter of months, adopting new payment apps and other modern technologies. Even well before the pandemic, several small banks made big bets on digital-only initiatives. Some of these are Cross River Bank, NBKC Bank, Quontic Bank, BankMD and Leader Bank.

Read More: How BaaS Turns Traditional Banks Into Digital Deposit & Loan Machines

New Model Reduces Expenses and Expedites Deposit Growth

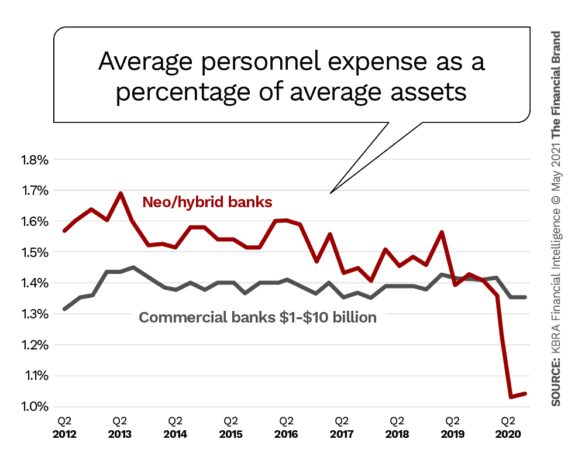

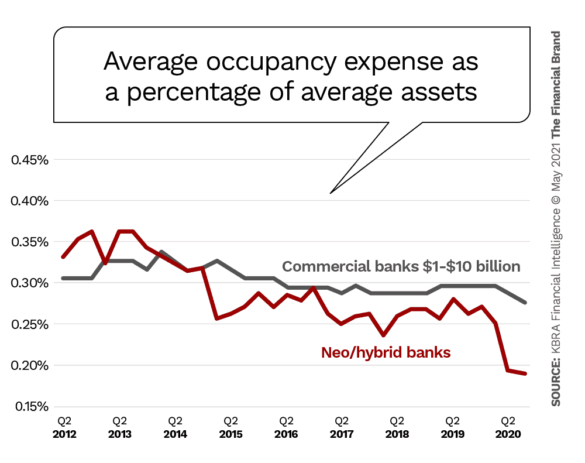

While innovative thinking boosted by new technology enabled these hybrid banks to reinvent themselves and stay relevant, it has also reduced personnel and operating expenses by decreasing reliance on physical branches. KBRA reports that the hybrid bank group has significantly lower average personnel expenses and average occupancy expenses as a percentage of average assets, compared to traditional banks with revenues between $1 billion and $10 billion.

Small financial institutions are not only reducing costs but also finding new revenue opportunities by offering banking-as-a-service, pursuing a digital niche strategy and other atypical initiatives. They’re also making marketing more productive, transforming customer contact centers, developing new channels and products, and enhancing risk management.

“On average, neo/hybrid banks invest more in marketing and technology than branch-based deposit gathering banks, which benefit from convenience/locale in deposit gathering and less competition for deposits in certain geographic markets,” KBRA states.

These banks are also using incentives to attract customers who otherwise might prefer to visit branches. In some cases, they use the savings of their lower overhead costs to subsidize premium interest rates for high-yield savings and checking accounts. For example, Axos Financial targets online savings with the highest yielding savings account of any bank in the nation, according to Bankrate.com. As of April 20, 2021 that stood at 0.61% APY — still low by historical standards, but well above the market average of 0.05%.

Shifting Sands:

As consumers increasingly move to digital and grow more aware of services outside their locale, branch-based models will need to compete more directly with hybrid banking models.

Read More:

- Small Banks Must Fight Harder to Stay Relevant in Payments Space

- 6 Cloud-Based Revenue Opportunities for Financial Institutions

- Can Nontraditional Credit Analysis Be Community Banks’ Path to Profit?

New Opportunities in Lending

KBRA found several neo/hybrid institutions have also implemented various technologies and strategies to maintain viability in a crowded lending marketplace. For example, while small banks have seen big players and fintechs eat away at their core clients of small businesses and high net worth individuals, some hybrid banks are now winning them back by blending new technologies with their traditional relationship management.

The SBA Paycheck Protection Program prompted many community banks to quickly enhance their lending platforms for expediency, KBRA notes. One hybrid player that already had such a platform, Cross River Bank, funded more than $6.5 billion for 198,000 business borrowers. (The bank has $9.7 billion in total assets.)

Hybrid banks are also finding new gains in other areas where smaller institutions’ share has been declining — non-real estate secured consumer lending and residential mortgage lending. Again, Cross River Bank is a leader in marketplace lending in this niche. By supporting leading fintech lending platforms including Kabbage (since acquired by American Express), Gusto, Upstart and Rocket Loans, it has realized risk-adjusted returns reflective of scale.

MetaBank and Axos Bank have partnered with tax service providers to offer consumers refund advance loans and other services. Many of these hybrid institutions have also redesigned relationship management via a “tech-supported-hub-and-spoke” model to eliminate silos between business segments. In addition, some community institutions are now looking to nontraditional credit analysis to find new market opportunities in the communities they already know.

KBRA says novel and innovative approaches to consumer lending will be increasingly necessary to compete with fintechs. In many cases, as indicated above, that means working with fintechs.

“The Covid-19 disruption has likely accelerated lasting changes in how banks interact with their customers, particularly in the branch delivery channel,” KBRA analysts conclude.