The good news for financial institutions out of the Covid-19 period has been an unprecedented gain in consumer satisfaction in a difficult year. The bad news is that the remote access enabled by a remarkable surge of online and mobile banking use produced a unique kind of isolation that left the digital-only consumers frequently feeling like their financial institutions weren’t communicating with them as well as when they visited branches.

There’s a give and take in face-to-face conversations that is lacking in mobile channels for the most part. A consistent finding from J.D. Power’s latest Retail Banking Satisfaction Study is that even those consumers who use branches lightly under normal circumstances feel there’s a dimension that mobile channels lack, according to Paul McAdam, Senior Director, Banking and Payments Intelligence.

This finding, while important to the further growth of digital banking, shouldn’t diminish the fact that the banking industry saw overall consumer satisfaction rise in the midst of extremely trying times. Satisfaction levels were stronger than usual even among consumers who feel worse off financially due to the mixed Covid economy.

Covid Service Was Recognized:

Nearly two-thirds of consumers surveyed by J.D. Power say their banks completely supported them during the crisis and nearly nine in ten say they would stick with their bank as a result of that performance.

The annual study is based on responses from over 94,000 retail banking consumers served by big banks (over $260 billion in domestic deposits); regionals ($55 billion-$259 billion); and midsize (less than $55 billion).

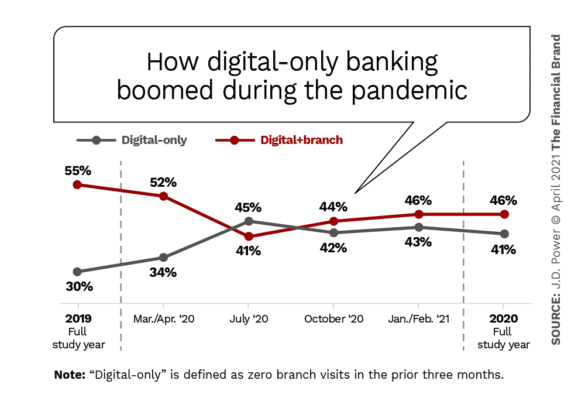

Digital-Only Contingent Leaps Ahead of 2019 Levels

A veteran bank data analyst, McAdam notes in an interview with The Financial Brand that broad measures of the industry typically advance a percentage point or two from year to year. Even amid the disruption and technological advances of the past decade, this has held true.

An Outlier of a Year:

The Covid boost to digital-only usage was beyond remarkable. In 2019 digital-only consumers represented 30% of consumers, versus 55% who used digital and branch. Over the course of 2020, digital-only users advanced by 11 percentage points, to 41%.

“The digital transition went very well,” says McAdam, particularly given so much else going on in banking at the time. Although that rate of increase is unlikely to be repeated over the course of 2021, J.D. Power analysts expect that much of the advancement in digital banking usage will stick and that some of the momentum of the Covid year will continue.

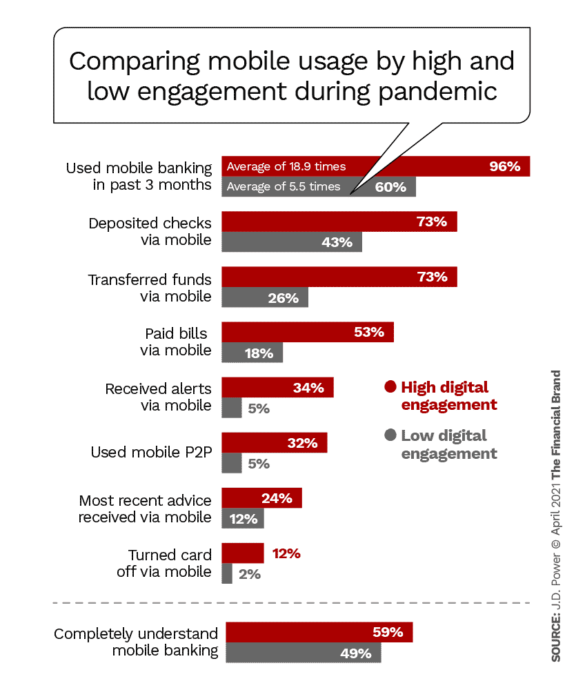

Part of what may help that momentum keep rolling is a greater effort to educate consumers in what they can do with digital channels, especially mobile banking. As the chart below indicates, while highly engaged mobile users made extensive use of certain mobile functions, there were others that could have been of great use that were barely touched by comparison. For example, only one in three highly engaged users tapped P2P payment capability in spite of a consumer trend towards contactless payments.

The reason for that can be seen in the final pair of bars in the chart — two out of five mobile users among the highly engaged don’t fully understand the service. And just over half of the low-engagement users don’t completely get mobile either.

( Read More: Consumers Are Less Happy with Digital-Only Banks (Here’s Why) )

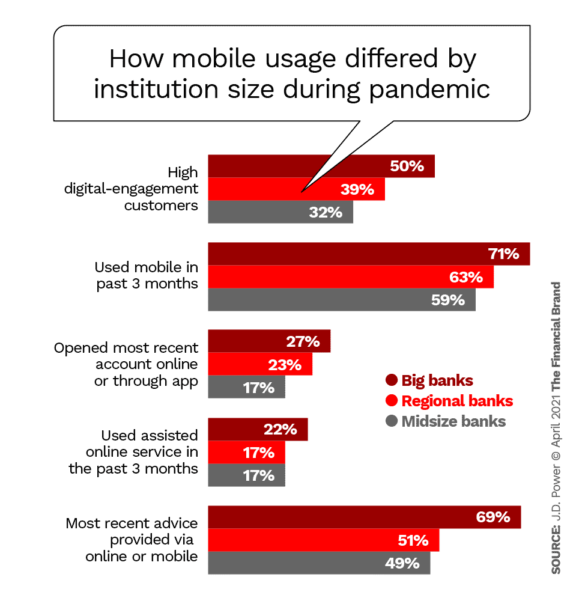

Generally the largest banks had an edge on other institutions in most areas of mobile banking usage. J.D. Power suggests that other financial institutions market and promote mobile deposits, mobile transfers, person-to-person payments and mobile billpay.

Read More: Mobile Banking Apps Failing in Key Areas of CX

Digital Channels Filled a Critical Covid Gap … But Something Was Missing

Being able to do so much digitally without stepping near a branch was a remarkable achievement. But as mentioned at the beginning of the article, digital-only left some consumers feeling out of touch.

McAdam explains that when a consumer visits a branch to transact they often feel like they receive advice and guidance on the fly, even volunteered by staff. “Do you need help with anything else today?” or “Did you know you can avoid fees like those?” are prompts that a staffer will provide. Online and mobile can provide prompts, popups, links and even live chat, but it’s not quite the same.

The survey found that digital-only customers were less happy than digital and branch consumers. Among the findings:

- They rate their provider “being far less friendly and less customer centric.”

- They are less likely to believe that their institution communicates honestly and with useful guidance.

- They tend to be unhappy about problem resolution, product knowledge, fees and advice.

McAdam says that while financial institutions have been communicating frequently via digital channels over the course of the pandemic, that communication has not always been effective, welcome or personalized sufficiently to make up for the lack of human contact.

A well-run contact center can somewhat fill the gap, he suggests, and J.D. Power research indicates that phone-based customer service has improved year over year, despite the stresses of higher call volumes during the earlier part of the pandemic. Training will help that channel supplement what consumers get from digital channels.

More Important Than Ever:

The importance of responsiveness overall will continue to be underscored in the year ahead. Even as reopenings proceed, and people feel some burdens lifting, many still worry about adding to savings and bolstering credit.

A worrisome trend was seen in the study’s data regarding the satisfaction of Generation Z. This group had the smallest gap between satisfaction expressed by digital-only and digital-plus-branch users. However, both categories of Gen Z consumers gave institutions weak satisfaction scores in multiple categories, including convenience, new account opening, mobile banking, ATMs and call centers.

McAdam says this trend has been seen in other work by J.D. Power. Gen Z uses digital channels more extensively than other generations and sees a broader range of apps. They aren’t that impressed by the banking industry’s efforts.

Communication Lessons from the Covid Period

The early days of the coronavirus crisis were a scramble for all businesses and communication became key for working not only with consumers and businesses but also staff. Financial marketers found themselves trying to find the middle way on multiple fronts. They tried to find the right tone for messages at each stage, as well as the kind of content people wanted. Finding the right channels for different messages, from Paycheck Protection Program loan availability to branch closings, challenged them.

Consumer satisfaction was highest with mobile app messaging in 2020, followed by communication at branches, phone, email, secure online banking sites, text messages and snail mail.

An important lesson emerges from this ranking. While text messaging has emerged as a growing customer communication channel, it is apparently not a panacea.

“Satisfaction with text message communication dropped like a rock. Our data reveals that satisfaction dropped sharply with the ‘relevancy’ and ‘frequency’ of proactive bank communication received by text message,” says McAdam.

During 2020 institutions sent out more texts, he continues, and “it’s clear some customers perceived the communications to be too frequent and less relevant.” He adds that many consumers found texts less clear than they should have been.

In Other Words:

By all means text if it’s critical, but think twice before using this channel and literally choose your words carefully. (And remember that some consumers pay for text messages.)

Yet it’s important to understand that frequency by itself is not the problem.

“Customers don’t mind increased communication, if it adds value,” says McAdam. He says messaging via mobile app and via secure online banking sites were more frequent in 2020 and yet satisfaction levels for both channels rose compared to the firm’s previous study.