BBVA attracted notice with its announcement to close the Simple and Azlo mobile banking apps. Simple was the pioneer of digital banking with around 100,000 customers when it was acquired by BBVA in 2014. I don’t know the number of Simple users at the time of the announcement, but I think if it was 12 million like Revolut has, we would have seen different headlines.

Without a doubt, the Simple app was the leading banking and budgeting product of its time. But let’s not forget that when it launched in 2012 it had practically no digital competitors. Today there are 21,000 fintech startups in the world, of which 8,775 operate in America, according to Statista. This is in addition to about 90,000 banks worldwide that are rapidly digitizing themselves.

We are living in a digital world. Out of a seven billion global population, five billion people are mobile users, according to GSMA Intelligence. There are three million apps in Google Play and App Store, which puts financial institutions at the center of an unbelievable global competition for the digital consumers’ attention.

Banks and credit unions need to make their digital service exceptional in order to stand out among that kind of competition.

Amid such competitive pressure, the rapid growth and achievement of the largest neobanks — Revolut, Chime and MoneyLion are three — can be perceived as a miracle. But, in the digital world, this is not really the case. Rather it is a consequence of certain patterns.

Behavioral Insight:

The peculiarity of digital consumption is that people are invested in trying new things, but they will switch very quickly if they don’t see significant value.

Even with digital games, it is not enough to have a good idea if the mechanics of the game are primitive. To become a bestseller, games have to be understandable, attractive, enjoyable and engaging to the majority of users. Therefore, gaming companies spend millions on digital architecture and game design.

Digital financial services are no exception. The success of digital financial products, putting it simply, boils down to the value that the financial product provides to its customers.

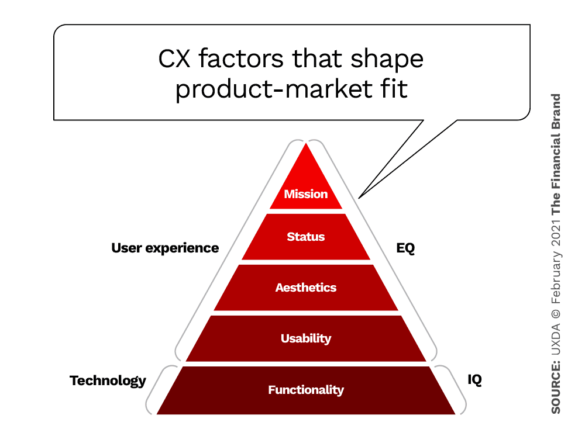

The value of financial services is in helping to manage finance and perform financial operations. So functionality is key. However, there are four more levels at which you can offer consumers value that will turn ordinary service into extraordinary. All four are closely associated with users’ psychological motives and emotional needs, which allows us to understand the anatomy of what creates demand and market fit.

The Psychology Behind Demand in Banking CX

The five elements of a successful financial product framework are associated with basic human motives derived from Maslow’s hierarchy of needs: Physiological, Safety and Security, Love and Belonging, Esteem and Respect, Self-actualization.

As we all know, competition is the main force stimulating the development of the product-value proposition. The greater the competition, the more financial institutions try to meet the needs of people and gain a competitive advantage. This means we can draw a parallel with Maslow’s hierarchy and assume that, as competition grows, companies will propel their products to higher and higher levels of human needs.

Here’s how we view the relationship between psychology and product value:

- Physiological Needs equate to Functional Value

It’s all about providing the desired result to the client through use of product features. - Safety and Security equate to Usability Value

The need for security is associated with the comfort of the person. Ease of use satisfies the need for control and ultimately creates a sense of security and confidence. - Love and Belonging equate to Aesthetics Value

Love and a sense of belonging are emotions. A product can influence emotions through aesthetics. - Esteem and Respect equate to Status Value

The need for respect can be satisfied with the help of the clear status value of the product or, rather, its agreement with a certain lifestyle. - Self-Actualization equates to Mission Value

The need for self-actualization is humans’ desire to maximize the realization of their capabilities. A product or service can inspire self-realization by offering a way to join an exciting large-scale mission that brings value to the world.

5 CX Insights That Shape Financial Product Success

With more and more financial products entering the market every year, competition becomes tighter and basic functionality is no longer enough to win over customers’ hearts. If we look at some of the fintechs, besides functionality, they also offer pleasant usability, aesthetics and personalization features that make a great customer experience. By doing likewise, your financial institution can come up with its own distinctive strategy of delivering value that surpasses your competitors.

All five elements that shape the product-market fit are accumulative and interconnected. It’s possible to reach the next higher level only by completing the previous one.

1. Functionality: Match Your Product With Customer Needs

Functionality is the foundation of all the following levels. It includes all the product features for basic user scenarios, such as checking balances, transferring money or mobile check deposit.

Most banks and credit unions have already provided their customers with basic functionality. The technical level of digital banking solutions is very stable. Functional innovations at this stage become less common and do not provide a key competitive advantage.

However, the rapid implementation of digital technologies, accelerated by the pandemic, has led to the disruption of the market monopoly of incumbents. Creating and launching a digital financial product has become relatively easy, and thousands of fintech startups have emerged or grown. This has started a transition to the next element of the framework: usability.

As digital solutions are constantly evolving, more and more well-thought-out multifunctional services are emerging that provide a wide range of features for their users.

Key Point:

It’s extremely important to align the actual customer needs of the specific service with great usability. Otherwise, a financial app overstuffed with unusable features can become a nightmare.

Action Plan

First, study the psychology, needs, wants, pains, fears and context of usage of your customers or prospects. Then craft possible solutions your financial product could provide.

Make sure that the features of your product fully meet the needs of your customers. Define the key user personas, create empathy maps for each of the user personas, define the Jobs-To-Be-Done (JTBD) and conduct a Red Route analysis.

Maintain a balance between user needs and the ability to satisfy them in an effortless and user-friendly way. From my experience, there have been situations in which financial brands aim to include a ton of modern functions in their products just because they believe it will make the solution stand out among the competition. But this might actually have an opposite effect, leading to user disappointment because of frustrating design.

Your customer experience research should determine whether customers require all of these modern functionalities or are seeking other features more important to their situation.

2. Usability: Empower Great Banking Customer Experience

The arrival of more convenient digital services has raised the quality of financial user experience and user expectations to a new level. Consumers have felt that online and mobile banking should be convenient and pleasant to use. Innovations in digital banking have moved from functionality to usability.

Reality Check:

Consumers now compare their digital experiences with big tech products with those they have with banking products. Often there is quite a gap between the usability of, say, Instagram and their banking app.

To satisfy the growing expectations of the post-COVID customer generation, it is not enough to provide simple functionality like the most basic online scenarios. You need to do it faster, more easily and more clearly than your competitors. Instead of just providing the opportunity to transfer money using a mobile phone by filling out a long detailed form, for example, you could offer the recipient the ability to quickly select a contact from their phone book and send money instantly.

Action Plan

Start with a thorough product audit: Determine the most critical elements of the user journey, go out and get user feedback, brainstorm the results and create solutions.

Conduct competitive research to develop an understanding of your competitors’ advantages and weak points. Review their products and discover how they position themselves in the market and toward their target customers.

Simple But Effective:

Exploring the ratings of competitors’ products on Google Play and App Store, as well as social media reviews, can be a great help in learning how users feel about these products.

This approach to banking CX design will help to avoid customer struggles due to the complexity of the product and difficulties that take extra time and effort.

Read More: Data Reveals a Surprise Driver of CX Satisfaction in Banking

3. Aesthetics: Create a Tailored Visual Identity That Wows

Many financial products still struggle with usability, while advanced digital services demonstrate not only ease of use, but also the aesthetics of their digital UI (user interface). These visually attractive products evoke more positive customer emotions than a template design.

Research confirms that consumers not only prefer more beautiful products but also are more forgiving of mistakes made by the providers of these products. However, we must bear in mind that the basic levels of functionality and usability should not be compromised, as they address the basic needs of users.

The ongoing massive improvement in the functionality and convenience of digital banking products creates the conditions for using the aesthetic value as a competitive advantage.

The new players entering the financial industry deliberately focus on unique and innovative design that communicates and highlights their brand identity. Most customers are tired of boring, complex and lookalike financial design. Tailor-made design is a better idea, providing users with something fresh and invigorating. Using it could mark the start of a new design era that skyrockets the market advantage of financial institutions.

Action Plan

Create a visual identity of your digital product based on the unique goals of your business, the essence of the brand and the character of its users. In this way, you form an emotional bond between your product and your customers.

Conduct design research, generate design, value and an emotional mood board and create the key design concept. This will help to prevent your bank or credit union from appearing outdated and boring and not differentiating from your competitors, and also help to avoid developing a product that doesn’t match the brand values or the standards of the digital age.

Create a digital product interface that’s unique in accordance with the visual identity of your brand. This will make the digital product delightful and allow it to stand out among the growing competition.

Read More:

- Consumer Frustration With Banking Apps and Mobile CX Lingers

- 5 Digital-First Strategies That Can Turn Banks Into UX Disruptors

- The Good and Bad (and Ugly) of Big Banks’ Mobile Sales Experience

4. Status: Personalize the Product Experience

79% of customers in the U.S. are certain that brands should demonstrate understanding and care toward their customers, and 89% are willing to engage with businesses that not only show care but go above and beyond that, according to Wunderman.

Even greater value and product-market fit can be achieved by connecting the financial product with the customer’s lifestyle. It means personalizing it for a specific audience such as VIPs, families, students or Millennials.

Status provides a powerful advantage as it personalizes the banking customer experience for a specific audience.

Note This:

Status value becomes an advantage only in the presence of appropriate functionality, usability and aesthetics. This is the only way to achieve ultimate customer-centricity. If these aspects are missing or do not match your users, then segmentation will not help.

Action Plan

The segmentation of digital banking services can be incredibly wide-ranging. For example, you can make an application for wealthy users, offering special privileges that serve as a symbol of high social status. Or you can create a financial service for families that centralizes family account management with a budgeting and control system.

What it Takes:

The key to becoming a successful financial institution post-COVID is having 100% focus on solving customers’ problems in the most effective way possible, instead of following a standardized scenario.

It requires true empathy toward the customers ─ getting to know them, feeling their pain like your own and delivering a solution that will make their lives better and easier. This calls for personalized, contextual banking experiences that can be empowered by artificial intelligence technology.

5. Mission: Create a Community Around the Ideology

The mission stage has not often been witnessed in the banking industry, until recently. Although long active in community support efforts, the industry has only recently begun to pay closer attention to customers as people and acknowledge their needs, pain and fears, so there’s still space for growth when it comes to mission.

A financial brand with a mission creates a community around its products and turns its followers into passionate fans. By maximizing its potential, it’s possible to turn design into the company’s ideology, a cornerstone of the business DNA, as Apple did. That company’s design philosophy reflects the principles of their world view and identifies authentic ways to convey this ideology through their products, ads and bonding with customers. This explains why Apple has established such a global impact with its products and became the world’s first trillion-dollar company.

Within such a business philosophy, a product or a service primarily becomes a representation of a company’s world view. This greatly increases the value that the customer receives and, at the same time, requires much more responsibility from the company. Not every financial institution dares to take this kind of risk because, in this case, design is directly related to the company’s reputation.

Action Plan

Provide the ultimate value through stating a mission with your financial brand that aims to make the world a better place and build a community around it. Look at design as your business ideology. What perspectives and opportunities does this open up, and what can you do to realize them? Do your digital products and your overall communication with customers convey that your brand truly cares about making their lives and the whole world better in some way?

These five CX stages are the way to truly empower the banking industry by creating demanded digital products that ease the lives of millions of consumers and increase the chances of digital breakthroughs for financial brands all over the world.