The general expectation of many experts was that the lull of the coronavirus outbreak during the early summer of 2020 would not last and that the return of cooler weather, school and holidays would bring a spike in cases. Data on the rate of new infections confirmed that the virus has roared back.

“We were experiencing about 100 to 125 new cases a day in the spring, which seemed like a lot at the time,” observes Sean Cahill, CEO of True Sky Credit Union in Oklahoma City. “Just in the last few days [late November], we hit 4,400 new cases a day,” he said in an interview with The Financial Brand.

Given numbers like that, you might think widespread branch lobby closures would be the norm again. But the consensus from interviews and research data don’t indicate mass closures. Instead, the industry has implemented a measured and well-honed response building on lessons learned earlier in the year.

That said, banks and credit unions are taking the challenge, if anything, even more seriously than in the first round, implementing new procedures and technologies to help keep providing in-person service to customers who prefer it.

Factors that Prompt Changes in Branch Access

There is a wide range of reactions from financial institutions depending on state and local COVID conditions. “In Texas, as a general rule, more branch lobbies are open,” says Brian Rivel, CEO of the research and consulting firm Rivel. “In New York state, generally, as well as in most cities, most branch lobbies are accessible by appointment only, whereas in more rural areas, walk-ins are allowed if customers are wearing a mask and, in some cases, they have their temperature checked.”

Two other comments illustrate the diversity of views and actions:

“We are not seeing significant lobby closures yet,” states Kevin Blair, CEO, NewGround. “However, I believe we are still about one-to-two weeks early [as of late November] on stay-in-place orders that will likely close lobbies.”

“What we are seeing for the most part is that community banks and credit unions, even with the recent surge in COVID-19 cases, are not closing their lobbies again,” states James Caliendo, CEO, PWCampbell. “As for the larger national banks, some of them have not reopened their lobbies and are relying on drive up only to service their customers.”

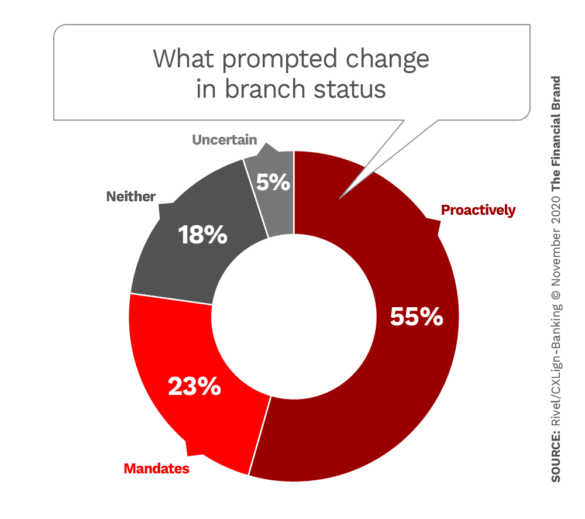

Those institutions that are taking steps are acting proactively more often this time, rather than waiting on government guidance. This came through in anecdotal comments as well as in a small sample of banks and credit unions surveyed by Rivel’s CXLign – Banking unit, shown below.

Closures in the first round were often reactionary and in some cases mandated, but in the second wave “we are seeing some of our clients close proactively and voluntarily, feeling more confident in their ability to communicate about lobby changes, to shift to drive-through service or ITM [interactive teller machine] service and video when needed,” notes Tom Kennedy, President, La Macchia Group.

Some of the verbatim responses from Rivel’s survey give insights as to the decision-making about branch closures and/or restrictions in this new round of outbreaks:

- “We will consider limiting access if there is an increase in COVID-19 positive cases in communities where our branches are located — if it becomes ‘red’ based on state criteria.”

- “We reviewed positive caseloads in the region/state and discontinued lobby access.”

- “It’s based on the level of local community spread, staffing availability and size of the office.”

- “The driving factor will likely be the guidance given by the governor’s office. However, the health and availability of our front-line workers could drive decisions regarding branch openings.”

Regarding the point about the size of the office, John Hyche, SVP, Principal, Level5, observes that “social distancing requirements are causing folks to rethink size,” and those out-of-favor “oversized” branches now have enough room to serve customers safely.

Read More: How People’s Changing Habits Will Impact the Future of Branch Banking

What’s Different This Time Around?

Two of the differences mentioned most often by respondents to the Rivel survey were the implementation of digital appointment scheduling and increased or improved digital banking capabilities.

Southwest and central Ohio, where Wright-Patt Credit Union operates multiple branches, have seen a significant uptick in COVID cases in the fall, prompting some significant adjustments to the institution’s operations.

“Our goal ever since the pandemic hit last spring has remained the same: To balance the health and safety of employees with our obligation to serve members’ financial needs. It’s been a tough balancing act at times,” says Tracy Szarzi-Fors, VP Marketing and Business Development.

In the latest surge of infections, Wright-Patt made several changes including the following:

- Basic teller transactions are allowed only at drive-through facilities.

- New membership applications are suspended (with some exceptions).

- Cash withdrawals limited to $5,000 without an appointment.

- Loans must be applied for online or by phone and will be available for current members only.

- Deposit accounts must be opened by phone or mail and will be available for current members only.

In Oklahoma, True Sky Credit Union was mulling over a plan to keep only half of their current nine branches open, according to Sean Cahill.

“If we get a COVID case in a branch, we’ll have to close it down, quarantine all the staff working there and do a deep clean of the facility,” he explains. “That facility may be down for days while we gather other employees to come in and work there. By keeping just half the branches open, it will make it easier to deploy resources to get an affected branch up and running again.”

Role of Technology Within and Outside the Branch

Although much of the technological impact of COVID-19 has been about the need to facilitate digital banking, as reported in The Financial Brand, other applications have emerged — several of them related to in-person banking.

When members of True Sky Credit Union enter one of its facilities, for example, they pause before a freestanding thermal mirror that scans the person’s core body temperature in less than two seconds, using infrared technology. Not only does the unit show the person’s temperature, it reads it out audibly, allowing others in the branch to hear it.

Cahill says customers like the audible feature. “They want to be safe too,” he says. “Their feeling is that we’re looking out for their health, not just their finances.” The CEO says that if a person’s temperature is above 100.4 — which has occurred several times — a staff member will ask them to go back out to their car. “We’ll serve them in their car so they won’t be exposed to anyone else in the facility.”

Cahill credits his wife for flagging the thermal imaging idea, which she had seen being used in other industries. Cahill contacted La Macchia Group, which was able to source and install the equipment for them. In addition to the thermal scanners, the build-design firm also suggested two advanced cleaning technologies for the credit union to use.

One is ultraviolet lamps, similar to those used in hospitals. These are switched on overnight when no one is around to bath the high-touch areas of the branches. Another is continuously self-cleaning surface covers made by NanoSeptic. These “skins” are placed on door handles, countertops and shared computer screens and oxidize organic material — including virus droplets — turning it into carbon dioxide. They are replaced about every 90 days, according to a news report.

“All this is table stakes now,” says Cahill, “We’ve got to be doing these things going forward to protect our members and employees — even once the vaccines come out. It’s not just about COVID — we’re in flu season now and there’s a value proposition to the membership to know that hygiene is important to us.”

ITMs, Mobile Video and Other Ideas

Interactive teller machines — basically ATMs with two-way video capability — continue to see increased interest. Wright-Patt Credit Union will no longer build a facility with standard drive-through units, according to Tracy Szarzi-Fors. Tey will use ITMs instead. Transactions go much faster with them, she notes.

Cahill says that True Sky is looking at ITM-only facilities in the future — such as walk-ups in heavy traffic areas — as a branch fill-in strategy.

Financial institutions can utilize unused parking spaces at traditional branches by converting them to curbside banking spots using ITMs, as an alternative to a typical drive-through arrangement, according to Level5. John Hyche points out that neither ATMs nor ITMs are actually contactless, however, and require diligent cleaning and/or use of antimicrobial films, similar to the ones mentioned earlier.

Mobile video applications are another way to enable consumers to conduct transactions remotely. Prompted by the pandemic, True Sky launched mobile video conferencing with document transfer, supplied by POPio. They introduced it in their mortgage lending unit because of the heavy documentation requirements. He says that while members are still on a learning curve with the technology, they are becoming more and more comfortable with it.

Finally, Wright-Patt uses a decidedly low-tech way to keep customers safe: a drive-up runner system. As Szarzi-Fors describes it: “When a member approaches the drive-through, they are asked the reason for their visit. If it is more complicated than a basic teller transaction, we will ask them to move to a parking space and will run the transaction into the branch for them.” She says employees use grippers and other tools to maintain distance between the member and the employee.