Small businesses have demanded unprecedented support and guidance while accelerating their adoption of digital technologies. Whether helping clients obtain Paycheck Protection Program loans or shifting to remote service delivery in the wake of branch closures, financial institutions have had nearly every engagement channel and relationship management process tested. Their performance in guiding small businesses through these turbulent times will impact their growth and performance for years to come.

Early feedback suggests small businesses will be more likely to rethink banking relationships going forward, while focusing less on traditional decision criteria such as proximity of the nearest branch. Greenwich Associates recently found that nearly 30% of surveyed small business owners had a lower opinion of their bank after seeking a Paycheck Protection Program loan, and suggested the number of firms searching for a new banking relationship may triple.

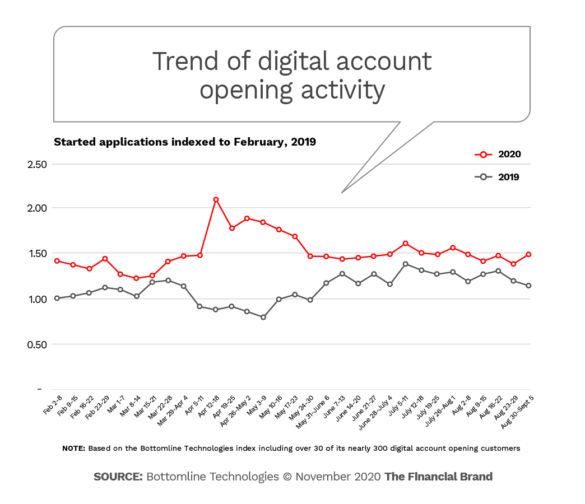

Meanwhile, a slowing economy has not reduced digital account opening activity. In fact, as shown below, since early February 2020 total volume across all application types is over 35% higher than it was in 2019. Online applications have continued to outpace last year by 20% in recent months.

Even after conditions return to something closer to normal, it’s clear small businesses will demand more personalized and frictionless engagement and will be more open to working with financial institutions who can deliver. Digital account opening can play a key role in driving intelligent engagement for both new and existing small business clients as part of a long-term, high value relationship.

Meeting the Unique Needs of Small Businesses

Many financial institutions fail to tailor the digital account opening experience for these increasingly restless small businesses. Instead they rely on a retail solution that too often lacks key capabilities and workflow support, or they offer a corporate client platform that overwhelms small businesses with unnecessary complexity.

Financial institutions can simplify and focus the application process on the needs of small businesses by:

- Delivering small business-specific workflows that capture key inputs and share appropriate disclosures and agreements for each type of business and application.

- Sharing digital “lockers” to organize the additional documentation required for many small business applications.

- Performing real time identity verification for the business as well as for beneficial owners and signers.

- Streamlining signature collection by giving multiple authorized beneficial owners and signers appropriate access, including email and text-based follow-up.

- Compiling all signatures, documents, identity verification results and other details into a single digital package to facilitate application reviews.

- Managing reviews including expanded anti-fraud and anti-money laundering checks through a single, integrated administrative console.

- Automatically provisioning approved applications to the core where appropriate.

The “on the go” nature of many small businesses also places a premium on capabilities including the ability to pause applications, to complete them in multiple sessions from different devices, and to submit them any time of the day or night.

With the unfortunate increase in fraudulent activity that is accompanying growing online adoption, fraud and risk management checks are also key to growing small business digital relationships. These include automated identity validation for businesses and individuals associated with each application, red flag and good standing checks with both private and government entities, funding risk management including secure and instant funding of new accounts, and embedded intelligence including machine learning to spot anomalies across channels which could suggest fraud.

Engaging small business clients with such a purpose-built digital experience enables financial institutions to differentiate their relationship experience from day one. Real-time tracking of key value drivers such as the time required to complete various applications and fallout rates at each workflow step is key to maintaining the advantages created by small business-specific functionality and workflows over time.

Delivering a Compelling, Multi-Channel User Experience

While the use of desktop browsers has grown recently as more applicants work from home, mobile devices continue to account for the majority of new digital applications. The growing need to engage small businesses across a variety of channels demands a responsive, mobile-first design which instantly adapts to the layout and capabilities of each applicant’s device. Applicants will expect key functionality such as photo ID and signature capture, document upload, and the delivery of consultative recommendations for relevant products and services regardless of how they engage.

Delivering a compelling user experience requires more than just the ability to capture applications though phones, tablets, and kiosks. Digital solutions must guide the user through what can seem like a complex and intimidating process, particularly for first-time digital applicants. As engagement expands outside of normal business hours and from new devices and locations, simple and intuitive workflows supported by consultative advice become critical. This includes checklists and context-driven workflows to ensure applicants complete only essential steps and can track their progress. Applicants should also be able to upload documentation and obtain signatures from multiple signers over several sessions if needed, and to “pick up where they left off” while easily tracking status and progress.

Additional Resource:

Driving Broader Digital Transformation

While some small businesses may turn to digital channels out of necessity, many banks and credit unions are targeting a larger opportunity to “make digital how banking is done.” Digital interactions increase service availability, shorten turnaround times and reduce cost, which creates significant value for both financial institutions and their clients.

Digital account opening can eliminate frustrating time delays caused by inefficient manual processes such as obtaining hard-copy signatures and tracking down documentation the applicant didn’t understand was missing. Such back-and-forth can often extend new account opening cycle times to weeks or even months, even for existing clients the bank or credit union should already “know.”

Tight integration with both the core and online banking is a key first step. Encouraging new clients to create online credentials when applying and to link directly to online banking after the application is complete and provisioned to the core can increase ongoing digital adoption. Also, existing small business clients should be able to act immediately on recommendations they receive during routine online interactions through “one click” access to pre-filled applications.

For more complex products and services, integration to commercial onboarding also plays a vital role in maximizing the scope of services for which straight-through processing can be achieved. Successful integration eliminates the need for applicants and onboarding teams to search for information that the financial institution already possesses. End-to-end tracking also helps everyone from small business owners to relationship managers to small business team leadership understand current onboarding status. It also gives internal users actionable information on delays and bottlenecks to drive client-specific intervention and ongoing process improvement.

Intelligent Engagement to Maximize Value

A wave of new small business applicants has driven growth not only in new online account volumes, but also in the number of applications that are started but never completed. These abandoned applications can represent 40% or more of total started applications. Likewise, retaining new digital relationships, particularly during the first year when churn rates are typically higher, is increasingly important as clients engage in new ways and are more open than ever to exploring new financial relationships.

Maximizing the value of digital account opening requires monitoring application activity to identify and re-target abandoned applications in a programmatic and timely manner. High-performing digital teams are able to re-engage applicants minutes or hours after they abandon an application mid-stream. They also understand the likely value of the re-targeting effort including the expected response rate and the estimated value of the new account or relationship, and invest accordingly in programmatic email follow-up or, for the highest-value abandoned applications, telephonic outreach.

Monitoring the ongoing behavior of new accounts and clients is key to maximizing retention for the most valuable relationships on an ongoing basis. Timely tracking of key risk indicators including balances, transaction volumes and patterns, online engagement, and service issues is critical for identifying churn risk in time to act, as is the use of machine learning to surface new and unexpected risk patterns and to predict future risk. This same data set and machine learning approach can also be applied to spot growth opportunities, such as re-engaging clients who are writing a high volume of checks from their new accounts but didn’t enroll in positive pay during the account opening process.

Driving Immediate Growth and Long-Term Value

An intelligent, omnichannel digital account opening process tailored to the unique needs of small business can extend an engaging “front door” to the flexible, frictionless online experience that clients increasingly demand. It can help create the differentiation required to maximize growth at a time when small businesses are re-thinking their banking relationships, and also play an ongoing role in achieving the scalability and efficiency required to maximize the value of this key market segment in an increasingly digital future.