The good news out of the social media world for traditional banks is that people see them as trustworthy providers of many services and substantial perks.

Unfortunately, that’s also a great description of a grandparent.

Fintechs, on the other hand, are seen as a concern when it comes to security and privacy, but they are seen as offering financial empowerment, and besides, they are cool.

That’s on the other end of the popularity scale from grandma and grandpa, and kind of like that exciting friend from high school you wouldn’t trust with your credit card.

“Digital and traditional banks are engaged in a fierce battle for customers,” states a white paper from The Economist Intelligence Unit. “Key to this battle between old and new is whether innovators can scale up and broaden their appeal faster than incumbents can innovate.”

In research sponsored by Temenos, the Economist Intelligence Unit developed a natural language processing model that read and digested over ten million online conversations in English about finance and banking appearing on the social platform Reddit from 2013 to present. (Most were from people in the U.S. and the U.K.)

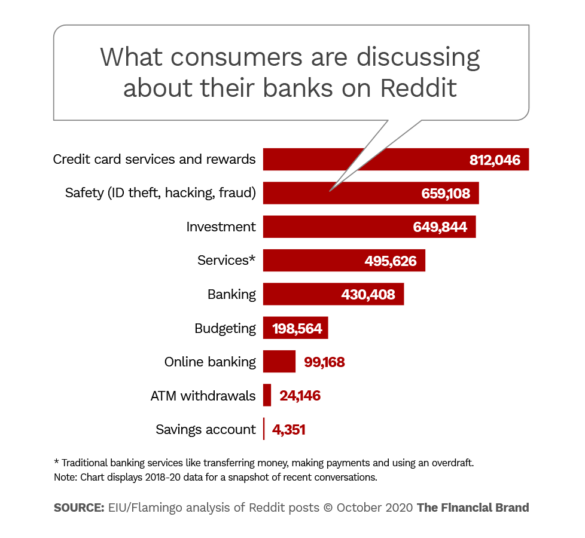

Reddit was used as a proxy for all social media conversations about personal finance because its structure best matched the way the research unit’s software worked. (The first chart included below shows the 2018-2020 portion of that analysis.) Reddit, symbolized by an stylized icon of an alien with a single antenna and red-orange circles for eyes, is a social news aggregation, web content rating, and discussion website founded in 2005. It is organized around communities of interest and members can vote entries up or down, which affects placement in the community as well as potential appearance on the front page. InfluencerMarketingHub.com ranks it #9 of social platforms in its list of 77 social media sites that marketers should know. It has 1.9 billion monthly visitors, versus #1 Facebook, which has 2.6 billion.

The research was conducted to take a reading on consumer attitudes towards the new players versus the traditional ones before more of the challengers develop primary banking relationships with consumers, according to Alexa Guenoun, Temenos’ President of the Americas, Global Head of Partners and Member of the Executive Committee.

What the Chatter is About Traditional Banks

Broadly, the research found that the specifics of traditional institutions’ usual lineup of products and services doesn’t get discussed much in the social platform conversations.

“Bank products have basically become commodities and people don’t talk about commodities.”

— Alexa Guenoun, Temenos

“They have basically become commodities and people don’t talk about commodities,” explains Guenoun. They tend to discuss what they can accomplish with the commodities — the car they are going to buy with a car loan, rather than the car loan itself. In a sense, predictions that banking products will become embedded in other transactions may already be a reality in many consumers’ minds.

The most popular topic for consumers discussing the offerings of traditional banks is credit cards, but often it is not the basic card functions themselves but the loyalty programs that the issuers offer. These made up nearly one out of four social conversations concerning banks, far ahead of many more basic matters.

“Here traditional banks benefit from their age and experience, having built up significant loyalty with customers (whose perks accumulate over the years), and leveraging the reputation and reliability needed to strike commercial partnerships with companies in sectors like air travel and hospitality,” the report states.

During the COVID-19 period some credit card brands pivoted travel and other loyalty perk programs towards more practical and immediate incentives to fit the times. It’s conceivable challenger banks could bring much more personalization and adaptation to the efforts. Some have already started offering points programs.

The second-ranking topic that people discussed in regard to traditional banks was safety. Many researchers have found that online safety is a key concern for consumers these days and people discuss it on social when something in the news brings it back to mind.

While customers of traditional banks talk about safety, the study found that there’s a degree of confidence in the traditional players that consumers don’t yet have in many of the challenger banks.

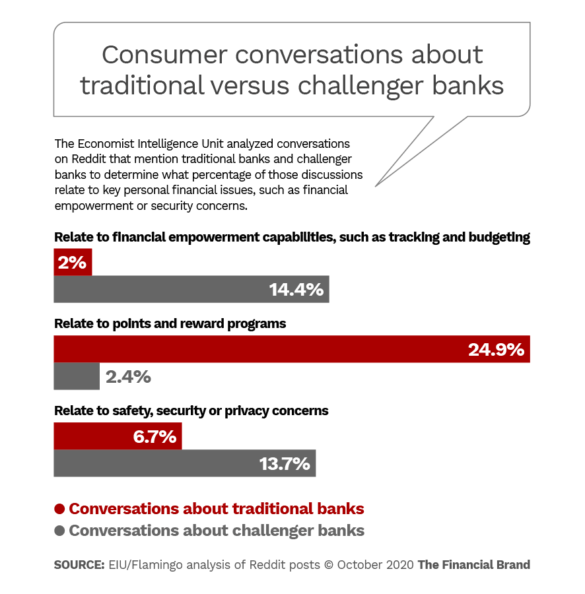

Concerns about safety, security and privacy occurred twice as often in regard to challengers as about traditional institutions, as shown in the third pair of bars in the chart above. “Many prominent challenger banks have slipped up on security and reliability, including through service outages and glitches,” the report notes.

“Clearly they are going to have to address the security issue soon because consumers are showing that it is a concern,” says Guenoun.

Read More:

- How Financial Institutions Can Keep Momentum Going in Digital Channels

- Fintech Buys Bank in Pursuit of Radical New Business Model

Financial Empowerment is Missing from Bank-Related Chatter

While there’s more trust in the traditional players, when it comes to financial empowerment, that is, taking control of one’s money life, banks hardly come into the picture, as the second chart shows.

Guenoun says this goes back to the issue of banking services being seen as commodities.

While community banks may bring some of this to consumers through personal contact and confidences, Guenoun says that “bigger banks have to learn how to get into their customers’ lives.”

Right now, except for the very wealthy, she suggests, larger traditional banks give an impression of arms’-length attitude.

“They are essentially saying, ‘I’m giving you a card, I’m giving you a checking account, I’m giving you a mortgage — and now you’re on your own’,” Guenoun explains. “And that’s why people are disengaging. They want something more interesting and they want their provider to be more involved — they want guidance. That’s why they are turning to challenger banks and fintechs.”

What the social monitoring indicates is that the providers that offer the tools and then help people use them to achieve their financial goals are the ones that get discussed.

While traditional banks both large and small have been introducing financial management apps at an increasing pace — many of them described in articles appearing on The Financial Brand, the fact that the fintechs and challenger banks seem to resonate more with consumers on social suggests that more aggressive marketing may be in order.

Guenoun notes, too, that as more fintechs and challenger banks obtain charters — Varo Money becoming Varo Bank is one example, and in late October 2020 SoFi received approval from the Comptroller’s Office for a full-service national bank charter — the line between the two industries will blur. (Varo is a Temenos customer.)

She points out that Varo Bank straddles both worlds. Through the new charter and federal deposit insurance it has taken on the trustworthiness of traditional banks. And yet it continues to retain the appeal of financial empowerment that was the hallmark of Varo Money, its predecessor.

“They are certainly trying to mix both,” says Guenoun, “and they are clearly targeting a younger population. And I think these are the ones who are going to thrive in the next few years.”