Crisis spawns innovation and the COVID-19 outbreak is now seen as having been a huge force for innovation as governments and institutions of all descriptions had to adapt to rapidly changing circumstances.

In banking, the pandemic’s sweeping impact has shaken up many fundamental assumptions and has changed the behaviors of employees, customers and other stakeholders, Accenture states.

In its Banking Technology Vision 2020 report, the consulting firm observes that even though the pandemic caused changes to occur in months that banks and credit unions expected to take years, many of the changes have been improvised and rushed by circumstances. Even so, these adjustments, including contactless payments, the shift away from branch transactions, digitized lending, and working from home will “be sticky well beyond the pandemic,” Accenture predicts. The challenge for financial institutions of all sizes is to think long-term as well as continuing to meet immediate needs for change.

The pandemic in many ways was an accelerant, not the originator, of massive shifts in consumer behavior and expectations. It forcefully surfaced such pain points as disjointed customer experiences and lack of personalization at a time when such capability simply became expected. As the report points out, many of the reasons financial institutions “might play it safe — failing to see demand for change, or being risk averse — are irrelevant in a world going through overwhelming transformation in such a short time.”

Accenture outlines four broad technology-driven trends reshaping the future of banking. These are:

- Increased consumer control over their banking experience.

- The potential for human/AI collaboration.

- Improvements in post-COVID customer experience.

- The need for financial institutions to build an “Innovation DNA.”

Key points of each trend are summarized here, amplified by comments from Alan McIntyre, Accenture’s Senior Managing Director – Banking, in response to questions from The Financial Brand. The report is based on a survey of 670 banking executives worldwide.

Trend 1: The Need to View and Engage with Customers as Partners

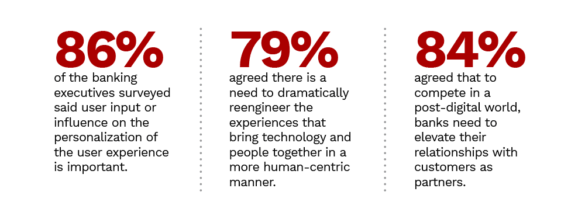

The effectiveness and impact of personalization depends greatly on how it is accomplished.

“Black-box personalization,” says Accenture, is common in the banking industry. But it leaves consumers feeling “out of the loop and out of control” over what is offered to them in terms of products and messaging — just the opposite of what personalization should be. Instead, personalization needs to encompass customer participation in some fashion — what Accenture calls “customer agency.”

Overall, a large majority of banking executives recognize the need for improved personalization.

“Consumers often find themselves confused by bank products and have difficulty understanding whether they are fit for their needs and how the fees and interest rates work,” McIntyre states. Two things are needed for banks and credit unions to get personalization right, he asserts:

1. Use consumers’ own data to help them make better and more informed choices. In this way, institutions can alert customers to potential fees or help them make the most of their spending, McIntyre states. For example: Are they leaving too much money in their checking accounts and should they open an instant access savings account? Should they be using an installment loan rather than a credit card to borrow?

2. Allow consumers to customize their own products within parameters set by a financial institution. For example, Barclays has allowed customers to change parameters on their credit card to better fit their needs. Or, for a CD, the customer could modify the term and early withdrawal penalty to have the CD meet their unique needs and profile.

“There is clearly a desire among consumers to feel their bank is on their side of the table and that there is a shared interest in success,” McIntyre believes. A true digital community, he adds, not only allows customers to learn from each other and share but would also have banks and credit unions being transparent about their own economics and interests.

That kind of transparency may be difficult for institutions to swallow. McIntyre acknowledges there would be a tradeoff between short-term profit and long-run customer value. “True personalization often means cannibalization of existing revenue streams,” McIntyre states. “Banks will need to educate their shareholders — the way big tech has — that revenue follows customer loyalty, share of wallet and increased retention.”

Read More:

- 7 Essentials of Digital Transformation Success

- New Tech Platforms Hold the Key to Retail Banking’s Future

- Inside the Strategy Behind BofA’s Digital Life Planning App

Trend 2: AI as a Banking Disruptor

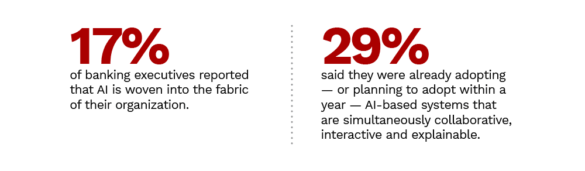

By now, many financial institutions use artificial intelligence tools in a variety of applications. This includes credit risk modelling, chatbots, fraud detection, and extraction of CX insights from data. Accenture calls all that merely table stakes and says that banking leaders are thinking about how they can use AI as an interactive collaboration tool.

“The banks that are unlocking the full value of AI look at it differently,” McIntyre states, “not only as a way to transform how businesses do their work, but also what their people actually do as well as how their business operates, delivers its services and interacts with customers. They are embracing AI as an agent of change across the organization.”

Based on the results of the Accenture survey, there is some work to do here.

In a complex process like mortgage underwriting, for example, the ability to use AI to interpret and highlight issues in documents can reduce the cost by thousands of dollars and speed the process. Trained loan officers would only look at cases that have already been flagged, McIntyre explains, rather than have to review every document at the same level of detail.

In other cases, the consultant says, AI can approach problems the same way as successful fintech disrupters: “Its judgment isn’t clouded by decades of previous experience or inherent biases, and it hasn’t yet learned what not to try.” This AI capability requires humans to direct and refine what the AI comes up with, McIntyre states.

All this is part of the growing field of “explainable AI,” according to Accenture, in which the output of previously “black-box” systems is de-mystified.

“Making AI explainable turns a human-AI interaction into a relationship,” says McIntyre. For example, if an applicant is denied a loan using AI, the system explains the reasons for the denial and offers the smallest number of changes the applicant would need to make to have the application approved, such as having more cash on hand or increasing annual income.

Trend 3: Necessity of Making Frequent CX Tweaks

During an analyst presentation, a Bank of America executive disclosed the astonishing fact that the bank had made more than 800 enhancements to its mobile banking app over the course of just eight months since the start of 2020.

While that figure may be atypical, the need for frequent and rapid updates to both digital and in-person banking products was acknowledged by banking executives in the Accenture Tech Vision survey.

“In the past, people may have been upset by banks repurposing smart devices, changing branch or contact center experiences, or rapidly introducing new features and functionality to apps and websites,” the report states. “Today they are more understanding.” The pandemic in fact has brought banks and credit unions a reprieve, “granting them leeway and creative liberty to use devices, apps and other digital channels to their full extent.”

“We believe that banks should not allow ‘the perfect’ to be the enemy of ‘the good’ in rolling out their omnichannel strategies,” McIntyre tells The Financial Brand. Instead, they should focus on delivering the engagements and experiences that help create connected experiences that “span different touch points in the customer journey.” Having a self-learning feedback loop that understands why customers couldn’t complete a task or a purchase online and then improving the process in iterative ways is critical,” McIntyre adds.

The report also points out that as banks and credit unions improve their mobile apps and other customer interfaces they should also leverage these investments toward improving consumers’ financial health and well being.

Leading financial institutions are upgrading their digital capabilities to establish more collaborative, trust-based relationships, McIntyre notes.

Read More:

- The Future of Banking: Tomorrow Will Be Radically Different

- Digital Transformation Demands a Culture of Innovation

Trend 4: Creating Innovation DNA

Accenture doesn’t mince words about the need for innovation in traditional financial institutions post-COVID:

“Yesterday’s expectations for innovation are out the window. Even though the stakes for innovation in banking were rising even before the coronavirus arrived, now a true culture of innovation is a matter of survival through, and beyond, the pandemic.”

Creating a unique “innovation DNA” has two components, the report states:

1. Maturing digital technology, including cloud-based applications that enable a growing range of applications. As the report states: Leading financial institutions are “decoupling applications from legacy infrastructure and moving to the cloud.” This allows APIs, microservices, data lakes and more to be run in parallel with legacy systems. Goldman Sachs, for instance, has built a platform called Marquee, which the company uses to decouple data from its respective data silos, Accenture states.

2. Emerging “DARQ” technologies. These are: Distributed ledger, AI, extended Reality, and Quantum computing. McIntyre acknowledges that it’s early days for most of the DARQ technologies other than AI, which, as noted above, is much farther along in banking. Yet the others are all already in use. 2019 Accenture research pegged the level of bank use of a slightly different list of technologies:

Which of these new and emerging technologies

is your bank investing in over the course of 2020?

AI 60%

IoT and sensors 53%

Quantum computing 37%

Distributed ledgers 31%

McIntyre insists that traditional financial institutions “can no longer hide behind regulation as a reason for holding back on innovation.” Regulators in most markets, he says, have become more flexible in enabling banks to take advantage of the latest tools and technologies, and in some cases are driving — rather than inhibiting — innovation.

That said, fintechs and other specialized players can often innovate at a faster pace because they are less inhibited by legacy technology, according to McIntyre. “It often makes sense for large incumbents to partner with fintechs to upgrade their core offerings with innovative products.”

For midsize and community institutions, McIntyre’s advice is to choose their vendors well.

“In the past, many banks and credit unions have bought bundles of products that have locked them into complex multi-year contracts and limited their ability to bring in third parties,” says McIntyre. In the future, he sees smaller institutions taking further advantage of API-driven products and services to build their own tech stacks so that they can have more control over, and align with, their business priorities.