Given the tremendous advance in analytic tools available and the processing power generated by cloud-based architectures, the banking industry needs to take a major step forward to meet the expectations of an increasingly discerning customer base. In short, the industry needs to move from using data to build great internal report of past events to using data to build great customer relationships and experiences based on future needs.

It is clear that the industry must move away from the siloed approach that has always defined banking, toward a model where the focus is on customer needs. This advanced analytic approach has the power to reinvigorate the relationship with customers while increasing satisfaction, improving profitability and building trust at a time when large and small competitors are providing new customer-centric digital solutions.

A report from Aite Group examines the state of marketing analytics, the data sources available, analytic techniques being applied, and how digital interactions with consumers will evolve in the future.

Marketing Trends

Most financial organizations realize they have a massive storehouse of data, but few know what data is important, or how to leverage this data for increased revenues and lower costs. And as channel proliferation increases, the ability to know what channels are the most effective and efficient to reach any individual consumer is getting more difficult. According to Aite Group, “FIs will have to figure out how to better insert themselves into a digital world and find unique ways to engage consumers in interactions based on their needs, life stages, aspirations, and account spending.”

Some of the market trends that marketing must take into account include:

- A need to generate customer relationship revenue

- Evolving consumer behavior and expectations

- A continued focus on improved operational efficiency

- The need for competitive differentiation through digital engagement

Differentiation Through Data

At a time when customers are interacting with their financial institution through multiple channels, the explosion in consumer data can help banks and credit unions generate key insights that can respond to new market trends and changing consumer behaviors. This can help organizations create better products and personalized experiences which can increase revenues and decrease costs. The results from a predictive marketing perspective will improve the ability to pull consumers in rather than push products out.

In the past, marketing analytics focused on what had already occurred … similar to looking into a rearview mirror. Today, analytics provides the opportunity to look into the future … similar to a ‘financial GPS’ … anticipating consumer needs. This is what is expected by consumers becoming accustomed to the predictive capabilities of giants like Google, Amazon, Facebook and Apple (often referred to as GAFA).

According to FIS’ 2016 PACE Index, 56% of consumers anticipate at least one life event with financial implications in the next 36 months. Nearly 75% of Millennials expect such an event during the same period, including tuition payments, a house purchase or the purchase of a car.

Interestingly, only one-in-three U.S. bank customers surveyed ranked their primary financial institution as the first place they would turn for major life events that required a financial investment. That leaves at least twice as many customers who may consider an alternative resource, particularly when it comes to investing or retirement planning.

Despite the desire to use “big data”, most financial organizations have had limited skills, challenges dealing with data sources and silos, had limited budgets and/or lacked organizational support. Today, many of those hurdles are gone since the capabilities of analytics tools have improved and the cost of these tools (and data storage) have dropped significantly.

Turning Data Into Insight

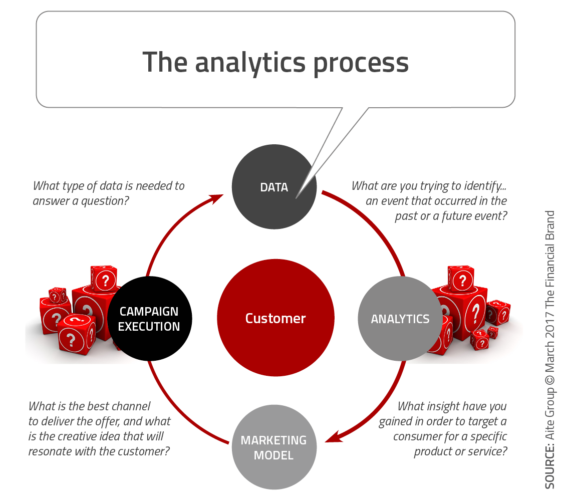

According to the Aite report, FIs first need to determine what data is needed to answer specific questions. They then need to determine what type of analytics are needed to address that question. Thirdly, the marketing model needs to be implemented to determine which consumer need a particular product or service. And finally, FIs must learn how to use the marketing model to determine how to execute a specific campaign – in real time.

In other words, select the right data, analytic process, marketing model(s) and channel(s), delivering the right message to the audience identified at the moment the need becomes evident … or even sooner.

Data Sources

Just like a house needs a good foundation, advanced analytics depends on powerful and predictive data to provide the foundation for maximum effectiveness. In the new world of AI, machine learning and cognitive analytics, many of the old, traditional sources of data aren’t as important, while new sources of data take on added prominence.

For instance, it is difficult to predict behavior using just traditional demographics (age, income, etc.). Alternatively, new social media and behavioral data sources help monitor key lifestyle changes, which can be the winning formula for the ‘financial GPS’ view of the customer.

Some of the data sources identified by Aite Group that financial service marketers need to include are:

- Channel preferences: Once a relatively minor component of marketing analytics, the channel(s) used by an individual consumer may be one of the most important data points in delivering an exceptional experience.

- Social media insight: With over two-thirds of consumers using social media, this can be a valuable source of insight into behaviors and life events.

- Mobile data: The amount of time on mobile devices continues to increase. Understanding how a consumer uses their mobile phone and their preferences of apps can be key in delivering the right solution through the right channel.

- Consumer ratings and reviews: What apps and services does a consumer like today? What do they like about the application? This insight can help build a solution that will resonate with a consumer.

- Bill payment behavior: Understanding who a consumer makes payments to, and how those payments are made, can provide valuable insights into how to serve the consumer with services that other organizations currently provide. The mission hasn’t changed even though the marketplace has … try to get an increased ‘share of wallet’ from the customer.

- Personal Financial Management: Understanding a consumer’s financial goals is one of the most important components of predictive analytics. Without understanding where a customer wants to go financially, it is almost impossible to help them get there.

- Geolocation: Before the massive acceptance and use of advanced mobile devices, the concept of providing solutions based on a customer’s location way nothing more than a marketer’s dream. Today, the ability to delver solutions based on location is one of the most powerful tools for financial marketers.

- Weather and other external elements: Applying analysis of weather and other external factors on top of the data points above provides an added layer of predictability of response for marketers. Obviously, if the customer is given the option of interacting on digital channels, weather is less of an issue, but other external factors, like news events, regulatory changes, etc. can all be part of the customer journey to purchase.

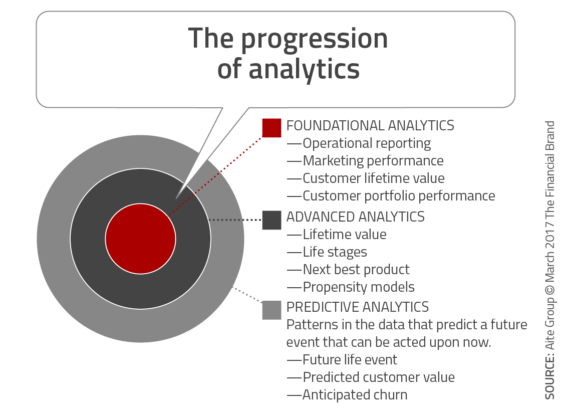

Moving From Foundational to Predictive Analytics

According to Aite Group, “Foundational and advanced analytics provides information about what has happened in the past and what marketers should do about it now. Predictive analytics has been primarily used in banking for fraud and risk, but marketers are starting to consider what role predictive analytics can play in marketing to consumers, building personalized offers, and delivering engaging, personalized consumer experiences.”

As we move from traditional analytics to predictive analytics, we can leverage new technology to deliver marketing messages to customers. Beyond direct mail, email, and even digital marketing, new touchpoints, such as chatbots, and voice-first interactive assistants will provide new ways to engage with a consumer. “Artificial intelligence (AI) that is fueled by predictive analytics, machine learning, and natural language processing will be the brains behind the face,” states Aite Group.

Predictive analytics is the future of financial institution marketing, predicting when a consumer will experience a life event or need a financial service solution. This advanced form of needs analysis, once only available to the largest organizations, is now financially and operationally available to organizations of all sizes.

The combination of predictive analytic tools and advanced digital delivery options can guide the customer to the best financial solution at the most opportune time … sometimes before the consumer even realizes they have a need. This level of predictability and advisory positioning will foster an improved relationship and increased loyalty, providing financial institutions with the differentiation required to compete in today’s, and tomorrow’s financial services marketplace.