Understanding the customer journey is at the foundation of being able to deliver the type of experience expected by today’s consumer. Disconnects occur when organizations are unable to link online and offline customer engagements, and when internal silos create communications that don’t reflect a customer’s needs and behaviors in real-time.

The New Marketing Reality report, produced by Econsultancy in association with IBM Watson Marketing, is based on a survey of more than 1,000 marketing, digital and ecommerce professionals. The findings illustrate many of the challenges faced by both financial and non-financial organizations, and the opportunities that new marketing tools provide in understanding the customer journey.

Some of the key findings of the 59-page report include:

- First-party data is the most available and the most used by organizations.

- Audience segmentation is a top priority, with 72% of firms using data for this activity.

- 67% of survey respondents use data for customer journey mapping, and only 54% use data for personalization.

- Most respondents remain in a channel-focused mindset, mostly caused by siloed organization structures.

- Over a third (37%) of respondents said that the customer journey is owned by a mixture of different departments and nearly a fifth (19%) said no-one has responsibility.

- Overall, less than a third (28%) of executives can tie their customer experience activities to revenue and/or cost savings.

According to the report, there is no dominant philosophy when it comes to tracking customer journeys online to offline. “Companies are largely using technologies that have been available to them for some time and of those, codes generated online for offline use (33%) or offline codes used online (22%) cover the bulk of respondents.”

In some cases, not having the right tools is an issue. In other cases, not knowing how to use the available tools is an issue. Two-fifths (42%) of the marketers surveyed agreed that they have the right tools, but didn’t know how to use them, while 50% stated that a technical barrier to progress is poorly integrated marketing technology.

Data, Data, Data…

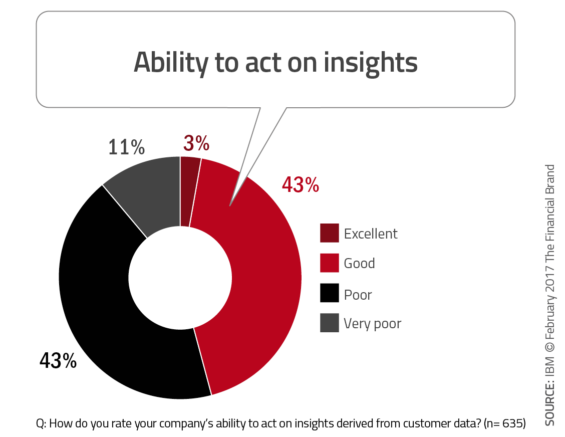

“54% rate their ability to act on insights derived from customer data as ‘poor’ or ‘very poor’.”

In travels worldwide, the availability of data does not seem to be the biggest problem for financial institutions. The real challenge is knowing what data to use for a specific objective and how to move from great reports to great customer experiences.

Read More: Data and Digital Channels Key to Customer Retention

As the sources of data continue to expand and the tools to leverage this data become more sophisticated, the challenges increase … as do the opportunities. When executives from all industries were asked about their company’s ability to act on customer data, exactly the same number of executives stated that their ability was ‘good’ as those who said it was ‘poor’ (43% each). Almost nobody thought they were ‘excellent’ (3%) while 11% admitted to being ‘very poor’.

When asked about data sources, first-party sources (website, customer data, explicit preferences) represented the vast majority of data used on average (75%), with second-party data (someone else’s first-party data) and third-party data (data from data providers) being less used (13% and 12% respectively). First-party data is the most available (and least costly), and can be a key driver of current customer value growth. However, this internal data is not nearly as valuable for acquisition efforts and may not be as helpful when trying to predict future behaviors of current customers.

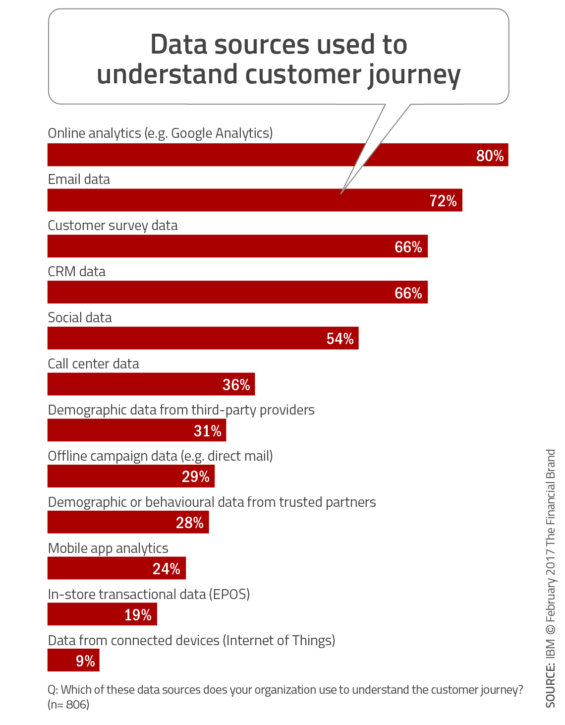

When organizations were asked about data used to better understand the customer journey, the most popular data source was online analytics (80%) with email data (72%), survey data (66%) and CRM data (66%) also being popular. Email was deemed important due to the ability to test timing and messaging, while CRM data provides the potential for contextual personalization.

Understanding the Customer Journey

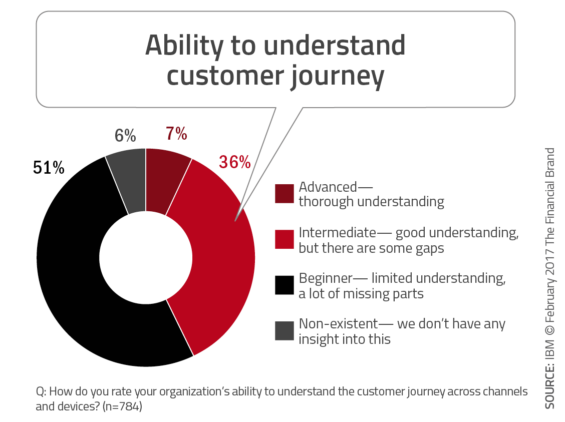

”57% of firms have a limited or non-existent ability to understand their customer journey.”

One of the most significant objectives of improved data collection and application is to better understand the customer journey. The traditional customer buying funnel no longer applies because it assumes customers and prospects follow a predictable path to purchase. With online and offline research and purchase options available, people will act the way they want to act, rather than sticking to a sequence designed by marketers.

The majority of firms surveyed use data to support customer segmentation strategies (72%). This is a standard practice for organizations of all sizes and in all industries. Of growing importance are customer journey mapping (67%) and personalization strategies (54%) that leverage cross-channel and behavioral insights. According to the report, “Personalization requires more than just the right name; it depends on context, content delivered at the right point in the journey. For personalization to work, companies need to be at least competent in journey mapping or analysis.”

The survey found that fewer than half of the organizations used marketing automation tools to drive communication. These tools are essential for real-time contextual marketing that can immediately respond to marketing opportunities in an ‘always-on’ manner. Further research from Econsultancy found that only a very small percentage of firms go beyond rudimentary triggers (attriters, birthdays, etc.). In other words, machine learning and artificial intelligence applications are nowhere near implementation stage except at the most sophisticated of digital organizations.

Bottom line, there is a significant gap between the ‘beginners’ and the ‘advanced’ practitioners of understanding the customer journey. In this research 51% of respondents were categorized as beginners, with a limited understanding of the customer journey. Just over a third were thought to have an intermediate understanding of the journey, with only 7% having a thorough understanding of the journey. While was reviewed for all industries, there is no reason to believe the percentages for the banking industry are vastly different.

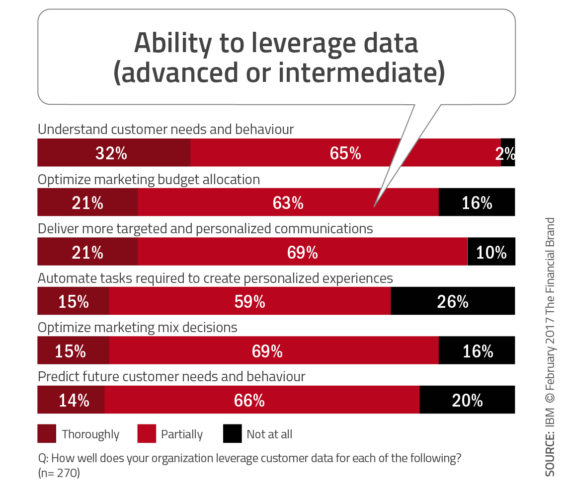

Among the firms that rated themselves as either ‘advanced or intermediate’, fewer than a third stated that they are able to thoroughly leverage customer data to understand customer needs and behaviors. A further 65% state they are partially able to do so. Only one-fifth (21%) of these more advanced firms were able to thoroughly deliver personalized communication, with only 14% having the ability to thoroughly predict customer needs.

Obviously, the capabilities were far less for firms considering themselves ‘beginners’. Predicting future customer needs and behavior was where the biggest differences were evident, with over half of the ‘beginner’ firms not being able to attempt this at all. While these less experienced firms said they could deliver targeted messaging, the ability to do this in an automated manner was non-existent.

According to separate Econsultancy research, “The majority of executives who consider email marketing and automated email marketing vital to growth still only use it at a basic level (i.e. welcome and transactional emails).”

Challenges and Barriers

”More than half of organizations cite organizational silos as a key challenge.”

The differences between the more advanced firms and beginners was also evident in the impact of challenges and barriers to success. More than half of the more advanced companies cited ‘siloed organizational structures’ (53%) as a key challenge, while 64% of the less sophisticated firms cited this challenge. IT bottlenecks were also a major challenge for all organizations with slightly over 50% of all firms noting this barrier.

The largest variances between the advanced and beginner organizations were seen in the categories of budget, leadership/ownership, internal skills and prioritization of advanced data capabilities. It was found that few in the advanced segment (16%) were challenged by a situation where understanding the customer journey was low down the list of business priorities.

Another challenge that has become key to understanding the customer journey is the ability to understand how consumers act in a multichannel environment. Today’s consumer doesn’t just use multiple channels, they move back and forth between them and use several channels at the same time. “Capturing this fluid experience is at the heart of most businesses’ digital transformation,” states the report.

When it comes to building an integrated, omnichannel view of the customer, 68% of respondents claim that they had “started to join the dots but had a long way to go”, with 8% stating they had succeeded at tying together data from multiple channels, technologies and databases. 24% of those surveyed don’t know where to start, had already failed or had no plans to integrate data across channels. Even those firms that considered themselves advanced stated that there was still a channel focus.

Retention vs. Acquisition?

Companies surveyed stated that, on average, 45% of their revenues were delivered by retention activities and 55% came from acquisition. Given that it is more expensive to acquire a new customer than retain a current customer, maybe it makes more sense to focus more on retention (and organic growth).

Interestingly, more experienced companies place equal focus on acquisition and retention, while 34% of them are more focused on acquisition and only 14% place more emphasis on retention. So-called beginner companies are more focused on acquisition, with 47% placing an emphasis on acquisition.

As first-party data accounts for 75% of a company’s data on average, and at least four of the top data sources for understanding the customer journey are first-party data sources – CRM, social, email and call center data – maybe less sophisticated firms would make a better investment if they focused more on organic growth.

The Best of Times and the Worst of Times

Despite the explosion of data sources including insights about everything from demographics to location, most marketers are having a very difficult time keeping up with changes in customer behavior and customer expectations that are being set by organizations such as Google, Amazon, Facebook and Apple (GAFA).

The survey found that many organizations may not be optimizing the data they already have. The potential of new data sources is tempting organizations to spend on expensive and channel-focused customer acquisition strategies when they should maximize their investment by focusing more on customer retention and growth.

According to the study, “Mapping those customer journeys without confusing the issue by introducing more diverse customer segments will allow companies clarity on their most effective strategies and allow them to tie journeys across channels together more cleanly.” In other words, work with what is at hand before confusing the issue.

The study continues, “Companies further down the customer journey maturity curve are likely to pull away from the laggards even faster in the future as they are in a position to capitalize on technologies such as machine learning and automation. Companies in catch-up mode need to find some way of overcoming immediate barriers that are preventing them from enjoying these advantages or they may find that the gulf soon becomes too wide to close.”

Jeremy Waite, Evangelist for IBM Watson Marketing states, “All in all, the current state of marketing is both ‘the best of times and the worst of times’. Yes, we are facing some difficult challenges, but within these challenges lie great opportunities to build better customer experiences and deeper consumer relationships. There has indeed never been a more exciting time to be a marketer.”

About the Report

This report is based on an online survey of more than 1,000 client-side (in-house) marketers from across different industries. Information about the survey was emailed to Econsultancy’s user base of digital professionals and marketers, and promoted online via Twitter and other channels during October and November 2016. The report is available for download after registration.