What are the greatest challenges, opportunities and concerns for the banking industry in 2017? How will the strategies being planned help organizations meet the needs of a changing consumer?

An annual study from Computer Services Inc. (CSI) delivers insight that can help financial institutions be better prepared for dealing with an industry in transition. The report analyzes feedback on 10 questions answered by 163 banking executives, representing institutions of various asset sizes and geographic locations.

Here’s a summary of this important report.

Overall, financial institutions seem relatively optimistic that the U.S. economy will remain strong in 2017. Even with recent and projected rate hikes, survey respondents believed small business, commercial and mortgage lending will remain healthy, with fee income being a growth opportunity over the next 12 months. Optimism is also reflected in projected increases in spending for customer experience initiatives.

That said, there are still challenges related to growth, profitability, security and compliance. An overarching challenge is related to being able to deliver a positive customer experience across channels.

Most interesting in this year’s report is the apparent disconnect between challenges, opportunities, spending and strategies in 2017. While there is a desire to grow revenues by delivering an enhanced omnichannel customer experience, some of the strategies to achieve this goal could be questioned, creating a banking customer experience paradox.

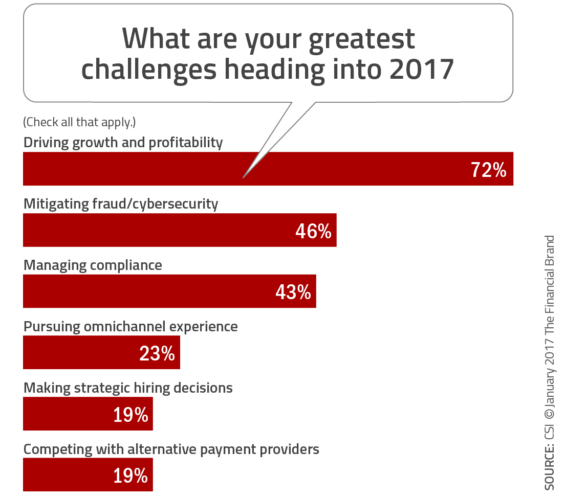

Growth and Profitability Remain an Ongoing Challenge

Similar to 2016, growth and profitability was named – by an overwhelming majority – as the number one challenge to the banking industry for the upcoming year. Nearly three-fourths (72.2%) of banking executives surveyed saw growth and profitability as their greatest challenge.

Not surprisingly, the second most mentioned challenge was around mitigating fraud/cybersecurity, followed by managing compliance. The importance of security rose in relationship to other challenges this year. As most institutions know, the challenge of keeping up with security and compliance issues is greater for smaller organizations.

It was interesting that “pursuing and omnichannel experience” was only mentioned by slightly less than one-quarter of the respondents (23.4%), given the significant attention given this objective in other industry surveys. This could be related to the term “challenge” in the question.

It is important to note that, while the industry continues to be concerned about growth and profitability, net income, net operating revenues, interest margins and deposit growth have all been positive in recent quarters. While the impact of the change in President is still far from certain, slow rate hikes should help most institutions.

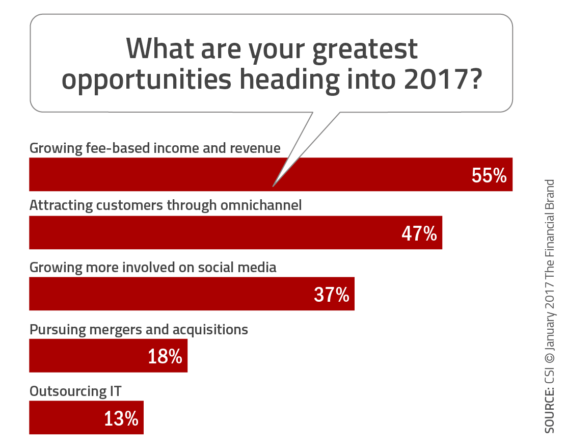

Growing Fee-Based Income Still Provides Opportunity

While a great deal of emphasis has been placed on growing fee income over the past several years, most bankers believe there is still work to be done in this area. More than half of the respondents to the CSI survey (55.1%) listed fee-based income and revenue growth as an opportunity in 2017.

The acquisition of new customers through omnichannel initiatives was the second most mentioned opportunity in 2017, at 46.8%. Given the challenges mentioned by bankers in implementing a strong digital acquisition strategy, it will be interesting to see if the industry can capitalize on this opportunity.

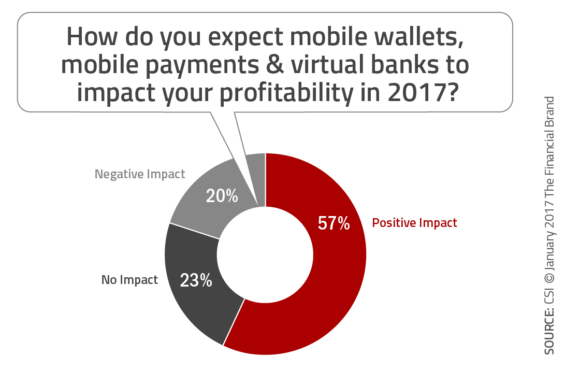

Impact of Non-Traditional Services Positive for Third Year in a Row

When respondents were asked about the impact of services like mobile wallets and mobile payments as well as virtual banks on profitability, a majority expected a positive impact. In fact, the percentage seeing a positive impact grew from 40.8% in 2016 to 56.3% this year.

As other studies have shown, the revenue and new business potential from these services and partnerships are far from optimized. In fact, while the awareness of mobile payments and mobile wallets continues to rise, the usage levels are still below 20% on a transaction basis. Usage levels may increase in the upcoming year, however, as EMV usage increases and as consumers become more comfortable with digital security initiatives.

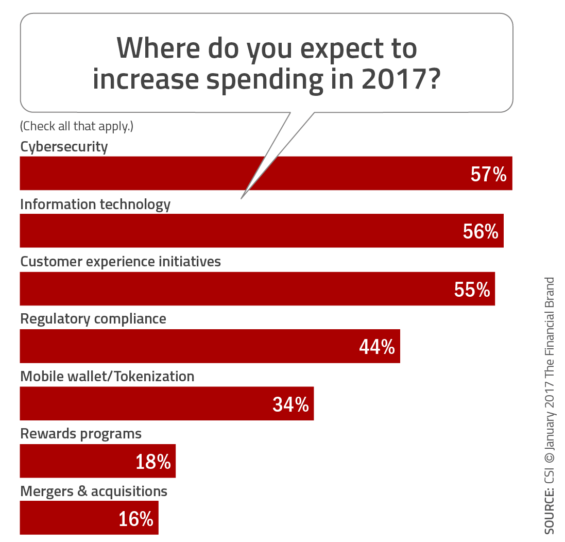

Cybersecurity, IT and CX Spending to Increase in 2017

When CSI asked respondents which areas will get increased spending in 2017, the three areas that were mentioned the most were cybersecurity (56.7%), information technology (56%) and customer experience (CX) initiatives (55.3%). Given the increase in cyber attacks, the need for core system upgrades and the focus on an improved customer experience, these priorities are not surprising.

Aligned with the challenges indicated by bankers who responded to the CSI survey, spending on regulatory compliance is also expected to increase in 2017. The impact of this spending was more dramatic as smaller institutions than larger organizations.

“In a crowded marketplace, financial institutions must prove their value to the customer, which includes offering service experiences on par with other providers, especially those outside the banking industry,” said Steve Powless, chief executive officer for CSI. “Banks must deliver services that allow customers to access financial services where and how they want, which means they will need to focus more of their attention and investments on technologies that directly affect the consumer.”

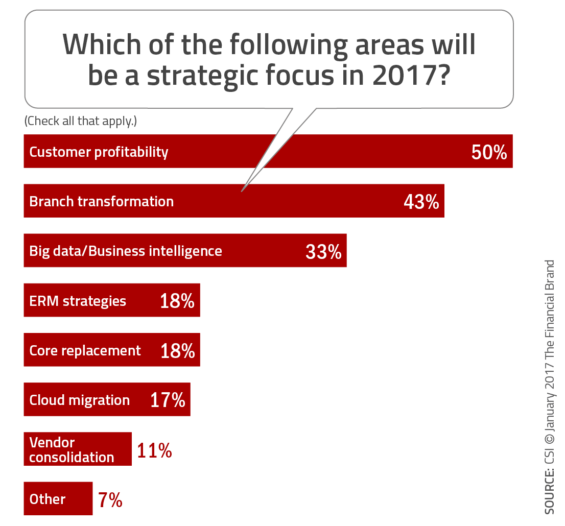

Strategic Focus: Customer Profitability and Branch Transformation

There are some interesting dynamics around where bankers wanted to focus strategies on in 2017. While the respondents to the survey ranked ‘Customer Profitability’ as the primary strategic focus (50.4%), it is unclear if the respondents believe this should be achieved through lower costs to serve or increased revenues.

In the past, an informed observer would point towards cost reduction as the way most banks increased customer-level revenues. Going forward, there is a greater opportunity to increase revenue through improved share of wallet and enhanced services if customer data is leveraged effectively (the third most mentioned strategic focus).

With respondents mentioning ‘Branch Transformation’ as the second most important strategic focus for 2017, it could be questioned whether this would be the best deployment of energy given the current state of mobile and online banking. Retraining branch employees, changing physical spaces and integrating digital technologies may be important, but most likely not at the expense of building better digital account opening processes or new mobile banking platforms.

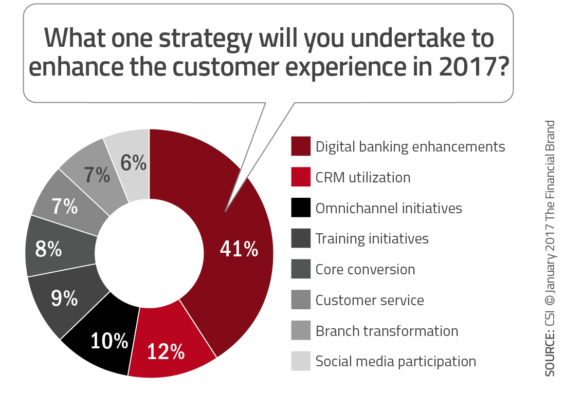

Customer Experience Paradox?

The importance of a positive customer experience can’t be debated. A good experience assists in acquisition, growth and the loyalty of a customer base. The challenge is in the definition of a positive customer experience and the application of resources toward that goal.

When respondents to the CSI survey were asked about the strategy they would pursue in the next 12 months to enhance the customer experience, an overwhelming percentage (41%) mentioned ‘Digital Banking Enhancements’. The next most mentioned strategies were ‘CRM Utilization’ (12%), ‘Omnichannel Initiatives’ (10%) and ‘Training’.

The paradox exists when we look at the high spending increases anticipated for branch transformation against the low value placed on this strategy (only 7% of respondents listed this as a customer experience strategy). This points to the importance of reevaluating branch investments at a time when digital banking investments may have the greatest impact.

The CSI Banking Priorities 2017 Executive Report continues to be an excellent barometer of where the banking industry is headed and how it intends to get there. A significant question raised by evaluating the responses to this year’s survey would be whether branch transformation efforts should be positioned higher than digital and mobile banking investments?

With an improved customer experience and resultant customer profitability being the overarching objective mentioned by survey respondents, is a digital path better than a reinvestment in physical channels that are getting far less traffic?