For decades, personal financial management (PFM) has earned a poor reputation across the financial industry. Chances are that most consumers never knew the product existed as a tab within online banking, and for those who did, they may have experienced difficulties in aggregating external accounts. In addition, poor categorization rates and clumsy data practices added up to a negative user experience. All of this deservedly hampered the reputation of such products.

As we approach 2020, however, the old ways are changing. PFM products are set to shift so dramatically that they require a new framing, which we might call data-driven money management.

Data-driven money management (DMM) differs from traditional PFM in several ways.

- Seamlessly merges money management functionality with digital banking options.

- Increasingly incorporates flexible investment functionality.

- Enables companies to easily create visualizations for better business intelligence.

- Includes actionable benefits for consumers.

- Highlights an educational component to help users’ improve their financial behavior.

1. Merging Money Management With Digital Banking

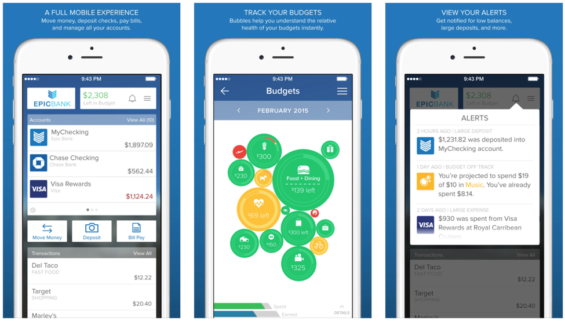

Consumers increasingly don’t have to dig deep into online banking to make use of money management capabilities. For instance, MX has partnered with digital banking providers to offer a mobile experience that fully integrates data-driven money management capabilities with digital banking. Users can sign in, add external accounts, track spending, visualize budgets, move money, pay bills, deposit checks, and more. In addition, the experience is built on a cross-platform framework, which makes updating on a range of device types far more affordable and effortless for client institutions.

By merging money management capabilities into the experience, financial institutions provide something that sets their digital app apart. They also make use of the data that comes from implementing such products, including accurate transaction categorization and an in-depth data analysis of internal and external accounts — data that can be used to improve market strategy at banks and credit unions.

2. Flexible Investment Functionality

After the global financial meltdown in 2008, Millennials grew wary of brands on Wall Street and searched for alternative ways to invest. At the same time, technological improvements made it easier for consumers to buck traditional options. As a result, a host of companies — including Acorns and Betterment — stepped in to give young consumers what they wanted.

One of these companies, GoldBean, analyzes users’ spending history and then lets them invest in the same companies they support each day with their spending habits. In this way, one’s personal spending becomes synonymous with long-term investing.

By analyzing spending data, GoldBean turns regular consumers into investors. As technology continues to improve and investment firms struggle with branding, we’re bound to see more innovation on this front going forward.

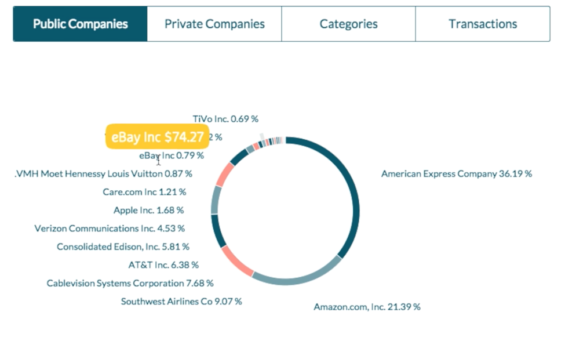

3. Visualizations for Better Business Intelligence

Data-driven money management enables users to create and customize visualizations in a way that wasn’t previously possible. To illustrate, Grow brings together a range of data points and displays them in a centralized dashboard so users can get clear and immediate insight into their overall financial strategy.

This information, which relies on aggregating financial data from a variety of sources, can be useful for banks and credit union employees because it allows them to make sense of end user activity and make smarter decisions.

In this way data-driven money management isn’t just about providing end users with a more compelling and seamless experience. The experience also leads to smarter business decisions from teams in financial services because the products are built on the foundation of accurate data.

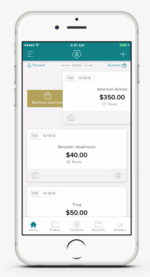

4. Digital Receipts and Cash Back

Digital receipt allocation with Spent

Everyone who’s had to wrestle with personal and business expenses knows how tedious the process can be. Data-driven money management helps solve this problem by offering actionable solutions. For instance, Spent uses account aggregation to bring a user’s transactions into a single view where everything can be sorted into personal and business categories. Users swipe right for business and left for personal.

In addition, each transaction is associated with a digital receipt, making it easy to get reimbursed for business expenses. Spent also brings all transaction data into a central view so users can see where their money is going month to month. Finally, Spent gives cash back rewards to users, with a focus on airfare, hotels, and rental cars. This way the company solidifies its solution for people who are constantly on the move for business.

5. Financial Education

Companies that create money management experiences have started to add an educational component — a strategy that is sure to stick. For example, SelfScore seems to just be a credit card for international students, but beneath the surface it offers a data-driven money management component. Within that component there’s a whole section dedicated to financial advice.

In this section, SelfScore guides their users on the basics such as how to open a bank account, how to review a credit report, and ways to improve your credit score. They also get into more complicated topics such as how to fix an error on your credit report.

This combination of digital tools and advice is a common theme from companies that offer data-driven money management. It’s a trend that’s sure to continue into the future.

The Future Is Integrated Data

Each of these solutions have been built on a foundation of data. What’s more, each solution aims to integrate the data throughout the experience, almost behind the scenes.

As data-driven money management continues to evolve, we can be fairly certain that integrated data will continue to play a bigger role than it has previously. Whether through APIs or through collaborating in other ways behind the scenes, data-driven money management will blend seamlessly with the user’s overall experience. Ironically, it’s by quietly merging behind the scenes with the full experience that what was formerly PFM will be most useful to consumers.