A survey of senior-level executives in the banking industry reveals that traditional financial institutions are far less critical of the customer experience they deliver than consumers. The survey, fielded by TimeTrade, reflects a serious misalignment of strategic priorities. Consumers crave a more personalized experience from banking providers, but retail institutions think they are already doing a pretty good job. Banks and credit unions say it’s easy doing business with them; consumers disagree. Banking execs are looking at turning their branches into cafés, while consumers only want improved convenience in the form of extended hours and more remote delivery options.

The banking industry can’t keep this up. It’s time to ditch the excuses and foolish delusions. Banks and credit unions simply must respond to the rapidly evolving needs and expectations of today’s consumers. This starts with acknowledging all the faults and flaws inherent in an arcane delivery model, then putting a comprehensive digital strategy on the fast track.

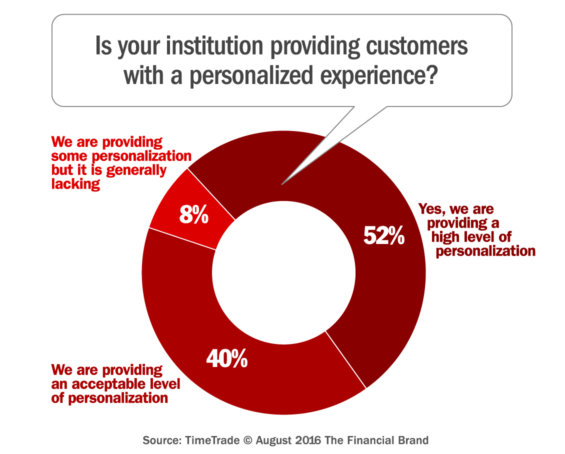

Banks Don’t Really Know What Personalization Looks Like

More than half (52%) of respondents in the TimeTrade survey said they feel their institution already provides a “high level of personalization” to customers. Another 40% say their level of personalization is “acceptable.” That means that 92% of financial institutions see no need to improve or push the ways in which they personalize the customer experience. Only 8% of financial executives confess that their personalization efforts are lacking.

Reality Check: Providing a “personalized” experience does not mean putting a customer’s name in an email, or greeting them by name when they walk into one of your branches.

These survey findings reflect a deep misunderstanding of what personalization looks like, and a serious lack of knowledge about what advanced capabilities are available in the field of personalization today.

First, you actually need to know someone before you can customize something for them, and this applies to everything from tailored suits and workout routines to banking services and retirement plans. But banks and credit unions struggle to understand consumers at even the most basic level. Most can’t even generate a single, aggregated view of their customers. If you can’t answer basic questions like “How many of our checking accountholders also have credit cards and a home loan,” you’re going to really struggle with personalization.

The truth is that banking providers are years behind the personalization curve, and it all starts with data. Just think about what retailers like Target have been able to do with data. Going all the way back to 2002, Target has been able to predict when a woman is pregnant in her second trimester, and then market to her accordingly. How is that possible? For decades, Target has been collecting massive amounts of data on everyone who walks through its doors. Target assigns each shopper a unique code — known internally as the Guest ID number — that keeps tabs on everything they do and buy. Every time someone swipes a credit card, uses a coupon, fills out a survey, calls the customer help line, visits Target’s website or opens an e-mail, Target logs the action in their Guest ID profile. Now remember, Target admits they’ve been doing this for at least 14 years! Meanwhile most banks and credit unions still can’t even stitch their basic customer data together.

Read More: Personalization in Banking – From Novelty to Necessity

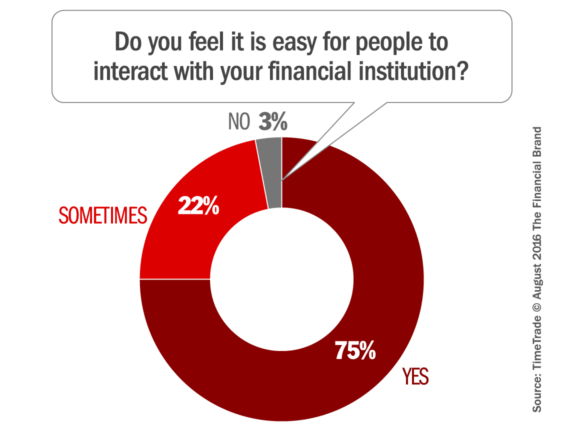

Sheesh, This Is So Easy!

Three out of every four financial executives (75%) in the TimeTrade study believe that it is easy for people to interact with their institution. 22% feel that it is easier in some channels but not in others. Only 3% say that it isn’t easy interacting with their institution.

This is pure lunacy.

Anyone working in financial services who thinks banking is “easy” is completely out of touch with reality. There are few industries that frustrate consumers more than banking. It’s rife with bureaucracy, paperwork and inefficient processes.

How hard is it to get a loan? How many pages is your loan application? How many trips to the branch do people have to make? How long does it take before an applicant is approved?

What about opening an account? Can someone open and fund an account without having to step foot in a branch?

How about your website? How many clicks does it take for consumers to find what they are looking for on your website? How deep do they have to dig?

Why do people who call the contact center have to repeat their card number after they’ve already typed it in?

31 pages of disclosure is not simple. Listing 14 different checking accounts with 39 possible fees is not simple. Banking terminology is not simple — HELOCs, FDIC, EHL, 401K, NSF, ARMs, IRAs. In fact, nothing about banking is simple. And yet this is what consumers yearn for the most. They want banking to be invisible. They want to spend as little time thinking about it as possible. Banks and credit unions that erroneously believe they are “easy” to do business with are ignoring a huge opportunity to differentiate their experience and their brand.

Read More: The Simplicity Revolution in Banking

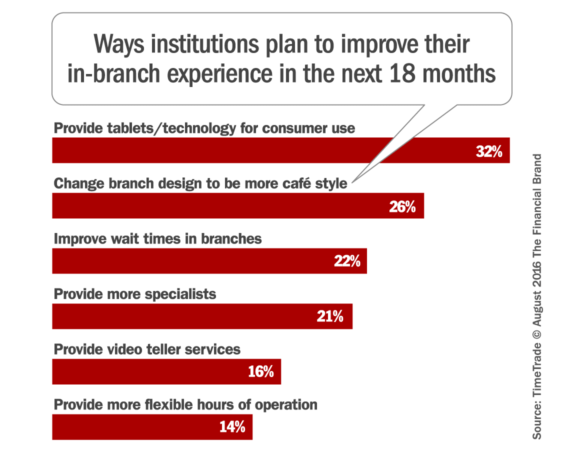

Shifting Priorities for Branches

As consumer needs evolve, banks and credit unions are trying to adjust the priorities of the branch channel to meet new consumer demands. But it seems that consumers are more ready and willing to ditch brick-and-mortar branches than banking providers are. More than half the financial institutions (52%) in TimeTrade’s study want their customers to balance in-branch visits against online and mobile contact.

This could perhaps reflect how far behind most institutions are in their digital capabilities. If banking providers aren’t prepared for the shift to digital channels because their technology investments have been insufficient, then you might understand why so many would prefer that people continue utilizing branches. Financial institutions, it seems, aren’t ready to wean themselves off the traditional branch-based delivery model.

The results from TimeTrade’s research reflect more disconnects between what financial institutions and their customers see as important priorities. 69% of consumers say they want the ability to bank after hours, but only 14% of the banking execs in TimeTrade’s study say they are interested in providing more flexible hours of operation. 46% of consumers want to pre-book appointments in branches and 18% would like to just stay at home and have a video call with a financial advisor. But these capabilities don’t seem to be a priority for banking providers.

It’s clear that traditional institutions are struggling with the role and relevancy of branches — How many? What size? Services? Staffing? In response, both banks and credit unions have been experimenting with “café style” branches for over a decade with very limited success. With the exception of Capital One 360 (ne: ING Direct) and a handful of others, most café concepts in the banking industry have failed.

Nevertheless, one in four (26%) of respondents in TimeTrade’s survey said they are planning to change their branch design to be more “café style” in the next 18 months, and 29% say they already have some “café style” locations. Another 18% are still waiting to see if this approach will be successful. Only 7% have concluded that branch cafés are a passing fad.

Yes, branches need to transition from the transaction factories they were in years past. Yes, branches can become more friendly and comfortable. Yes, branches should be reconfigured to facilitate greater engagement within the context of the new digitally-savvy world we live in today. But that doesn’t necessarily mean that you should try to turn your branches into a Starbucks hangout. People will never go to a branch “just because.” They visit a branch for a specific purpose, and prefer to do so as seldom as possible. In many cases, they are only using branches because they can’t get what they need through other channels (e.g., digital, self-service).

Read More: Free WiFi? Yes. Cappuccino Hangouts? No Way

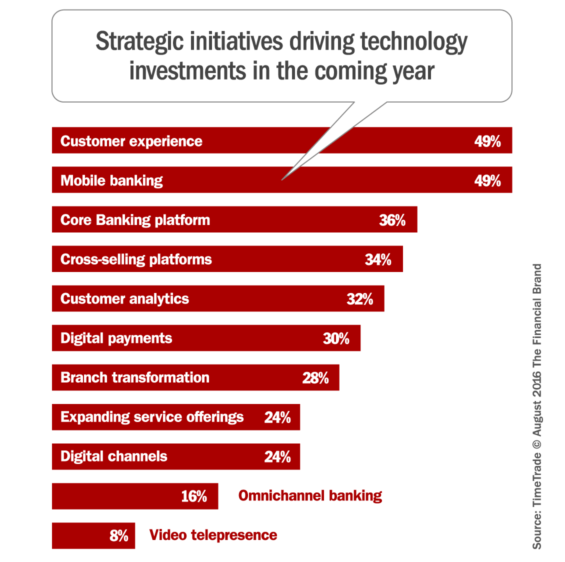

Investing in Tech to Improve the Experience

Fortunately, financial executives are willing to admit they have a few shortcomings, and are starting to take steps in the right direction. In TimeTrade’s study, customer experience solutions and cross-selling platforms were among the top technologies banking providers said they will invest in over the next 18 months.

When it comes to improving the experience, social (51%) and mobile (50%) are the top two areas banking executives want to focus on most. The trick, of course, is tying all these touchpoints together in a true, unified, omnichannel experience. Less than half (43%) of consumers feel that banks and credit unions today are providing a consistent experience across all channels.

What Banks and Credit Unions Must Do

It isn’t complicated… at least in theory: Banking providers must improve their digital capabilities. This certainly encompasses the overall experience — more technology, more access/convenience, and more self-service options — but it also involves data analytics. Financial institutions must learn how to build and dissect powerful data warehouses if they are to keep up with other industries. Data analytics is the key to segmentation, personalization and automation — the holy trinity of digital marketing today.

Banks and credit unions must also continue to push transactions out of branches and transform their retail locations into sales/service centers focused on high-value products. But again, this can only happen with an aggressive digital strategy.

Now of course, this is all much more difficult in application than it is to talk about. Everyone can agree that digital is the future, but it’s clear that most banking providers still have a long way to go. While it may seem like a daunting task — Where do we begin?!? — it is imperative to accelerate your digital strategy. If you don’t start today and get a plan on the fast track, you’ll only be that much further behind tomorrow. Most of the industry is already playing catch-up. Those who continue to delay and drag their feet are putting the very future of their institution in jeopardy.