Retail banking has never had such intense competition from both inside and outside the banking industry. While larger technology companies like Google, Apple and Samsung move into payments, an increasing number of smaller fintech start-ups are competing for individual service supremacy as the product set for banking becomes more and more unbundled.

The battlefield is no longer dominated by large, well-known legacy banking organizations competing on price or a physical delivery network. Instead, digital players are competing on the basis of consumer experience and design.

To understand the scale of the threat to banks, global experience design agency Beyond surveyed both US and UK consumers to test the readiness of consumers to switch to non-bank, online-only challengers. They also asked what consumers expect from the digital banking experience, to understand how banking can better meet their needs and avoid losing them to competitors.

The key finding in the dual set of white papers, Taking Friction Out of Banking: How Can Banks Improve the Digital Experience to Retain Customers in a Competitive Market? is that over half of the population of the US and UK would consider digital-only services for all their banking needs.

Those with complex financial needs (5 financial products or more) – often the banks’ most profitable customers – were even more receptive to online-only offerings (65% vs. 57%). In addition, consumers were more willing to consider digital-only options for payments and money transfers (79%) and checking accounts (77%).

In response to this challenge, banking needs to balance two competing priorities. On the one hand, banking needs to better cater to digital natives who expect the whole journey to happen on their phone. On the other hand, banking need to ensure the majority that may not be as digitally engaged have an optimal experience as well, regardless of the channel through which they choose to engage.

This balancing act introduces both complexity and the need to act fast. The experience delivered in the future will need to support different delivery channel desires, screen types, user journeys and need states. Unfortunately, each consumer follows a different decision path to purchase and loyalty.

Consumer Experience Expectations

The reason for this willingness to change financial services providers is that consumers are becoming digitally sophisticated as they get used to the intuitive, seamless experiences from firms like Apple, Uber, Google and Amazon. According to the research, “Today, a good experience is one that delivers the following fundamental elements: ease, speed, security, consistency and personalization.”

As expectations move up the digital experience pyramid, factors that were once impressive are now perceived as basic, entry-level requirements for a good customer experience. “Banking cannot move up the pyramid until they deliver against the basic fundamentals – and until they do, the difference between their customer experience and that of their rivals will only become starker,” states the research.

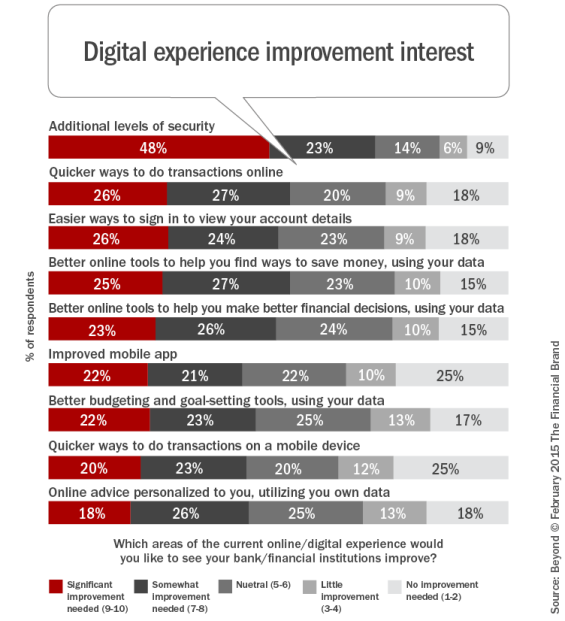

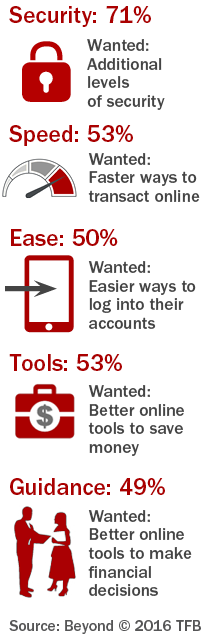

When the survey asked consumers to rate their current banking experience, the research found that consumers want improvement from their digital banking provider in the areas of security, personalization, speed and ease of use. It should be noted that these areas in need of improvement ranked at the lower, more basic levels of needs.

In the US, 71% of people wanted additional levels of security (vs. 65% in the UK), 53% wanted faster ways to transact online (vs. 56% in the UK) and 50% wanted easier ways to log into their account (vs. 52% in the UK). The challenge for the banking industry is that technology and fintech start-up providers are already delivering intuitive experiences that anticipate consumer needs, while banks are slow to deliver on consumers’ most basic expectations.

As most financial organizations have found, each of these digital experience expectations present design challenges.

The Security Design Challenge

As many banking organizations have found, the desire for enhanced digital security features often conflicts with the desire for speed and ease of use. For instance, while fingerprint technology appears to be a logical response to consumer needs, the research from Beyond found that for those who had not yet used fingerprint technology in the US, only 24% chose it as their preferred log-in method.

This doubled to 48% amongst those that had already used it (in the UK it almost tripled from 17% to 47%), illustrating that consumers tend to doubt technology they are not already familiar with. This challenge begs the question whether banking is doing an adequate job educating consumers on the features and benefits of their digital offerings.

The Ease of Use Challenge

The Ease of Use Challenge

The removal of friction from all consumer interactions is a worthy focus given the consumer desire for speed and ease of use. However, the research reminds financial institutions that when designing for speed and ease of use, there can be a negative impact as more customers worry that the simplified platform is not secure.

An example of this conflict of expectations is with voice authentication software, that already exists but is not in wide use as a result of customer anxieties around security components. It was found that if processes are too simple or seamless, the consumer worries their security isn’t being taken seriously.

Counter to the desire to remove steps from the digital process, the solution may be to design in some extra “time”. “Even if the authentication only takes a split second to execute, by employing some UX theatre during security checks and building in intentional delays, customers will feel more at ease inputting their personal data in the bank’s digital products,” says Nick Rappolt from Beyond.

The Personalization Challenge

In addition to the basics of security, speed and ease, many consumers also want the banking experience to respond to their individual needs with sophisticated online tools. The US research found that 53% wanted better online tools to help them save money, while 49% wanted better online tools to help them make financial decisions.

According to Beyond, “The ideal digital banking experience is not a ‘one-size-fits-all’ solution, as there is consumer demand for digital products that respond to them as individuals, delivering a personalized service based on their data.”

As with much within the digital design world, the desire for individualized communication and offers is a double edged sword. On one hand, the consumer wants their entire experience to be customized to their needs. Alternatively, they are equally concerned about any organization knowing too much about them … the “Big Brother” effect.

For instance, many consumers are wary of digital marketing tools such as retargeting when they may have been simply reviewing product alternatives on the Internet. Beyond suggests that if a bank does not clearly state that it is using personal data, or explain the benefit this gives to the consumer, there may be a risk of a perceived breach of trust.

When it comes to personalization and customization, it is important that banking organizations respond to consumer needs in a tailored and intelligent manner. From the consumer perspective, those households with the deepest relationships had the highest expectations on all fronts – from security to personalization. These consumers with the deepest relationships are the most likely to become frustrated with their current banking experience, leaving them wide open to offers from online-only competitors.

The Role of the Branch

Despite the fact that 57% of US consumers, and 64% of UK consumers, say they would consider going digital-only for all their banking needs, Beyond found that customers still value the branch experience. In fact, 77% of US consumers ranked their local bank or credit union as their first choice for financial offerings.

Based on this finding, it is still important for retail banks to design multichannel solutions, meeting digital demands, while retaining a physical presence. The goal should be to create a seamless, platform-agnostic experience that will be a differentiator against digital-only challengers … a digital solution that works in tandem with a physical delivery option.

While security, speed and ease are the foundation of an excellent digital banking experience, expectations are evolving so rapidly that banks are finding it difficult to keep pace. To remain at the forefront of the consumer selection process when considering financial services partners, banking must continue to innovate and evolve while leveraging the strengths that set them apart from digital-only offerings.

By combining the availability of physical presence with improved digital capabilities, the banking industry can offer the best of both worlds – blending physical with digital, serving a large consumer base with personalized offerings and a history of trust and security.