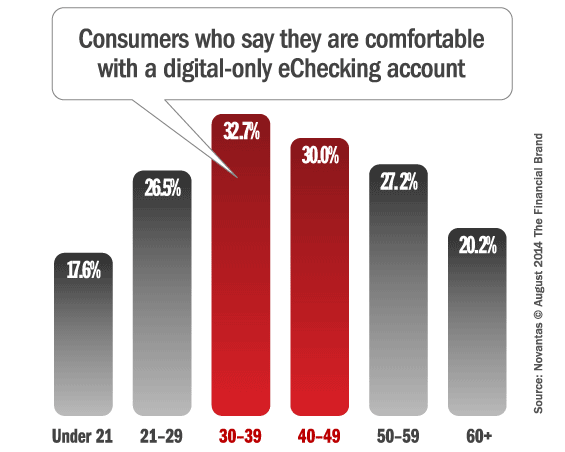

In a recent BankChoice Monitor survey, only 24% of Gen Y consumers currently shopping for checking accounts are comfortable with an account that requires they only use electronic channels like mobile banking and ATM machines, compared to 33% of Gen X consumers aged between 30 and 39. In fact, even checking account shoppers aged between 50 – 59 are slightly more likely to be comfortable with these types of checking accounts.

Some traditional institutions offer “e-Checking” accounts similar to direct banks like Ally — free, provided that customers receive statements electronically and only use electronic channels for their transactions. It’s clear why these accounts appeal to banks: customers cost less to service than customers who visit branches and call contact centers. Marketers typically target this product towards younger consumers, but the sweet spot for these e-Checking accounts is really Gen X consumers.

Characteristics of Gen X Consumers Comfortable With E-Checking Accounts

Most will set-up direct deposits. Two-thirds Gen X shoppers comfortable with eChecking plan to set-up a direct deposit with their new checking account. Twenty-eight percent report that they’ll have more than $2,000 in direct deposit per month.

Slightly lower average incomes. Only 20% of Gen X checking shoppers comfortable with e-Checking accounts report earning $100,000 or more, compared to 23% of Gen X checking shoppers who aren’t comfortable with these types of accounts. Higher income shoppers ($200,000 or more a year) comprise this gap – only 2% of high income shoppers are comfortable with e-Checking accounts.

Evenly split by gender. Overall, the survey indicates that more women are currently shopping for checking accounts than men (52% to 48% respectively). But men are slightly more comfortable with e-Checking accounts, evening out the percentage to 50%-50% male/female split for shoppers comfortable with e-Checking accounts.