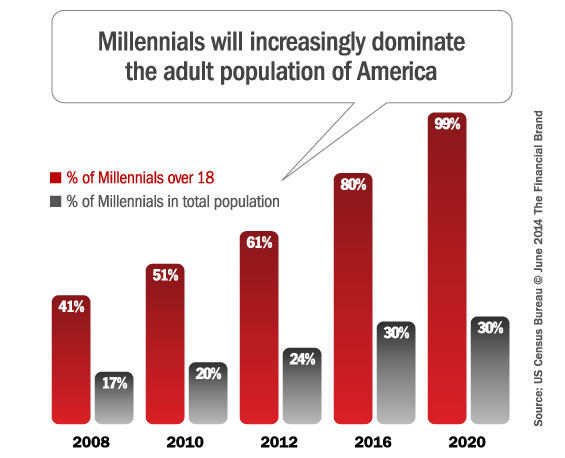

By 2020, millennials will comprise more than one of three Americans and by 2025, they will represent as much as 75% of the workforce. Almost all millennials (88%) do their banking online and half use their smartphone to bank. This leads about three-fourths of millennials (73%) to be ‘more excited’ about a new offering in financial services from Google, Amazon, Apple, Paypal or Square than from a traditional bank. Can banks and credit unions afford to ignore these trends?

Read More: Millennials Find Banks Irrelevant

According to an Accenture survey of nearly 4,000 retail bank customers in the U.S. and Canada entitled, ‘The Digital Disruption in Banking,’ consumers are more likely than ever to bank without branches and consider a non-traditional provider. The idea of “convenience” in banking is shifting away from branch locations and toward digital products and services that mesh with consumers’ mobile-empowered lives.

Key findings of the study:

- 27% of consumers would consider a branchless digital bank if they were to leave their current provider

- 71% of U.S. consumers consider their current banking relationship as merely transactional

- 51% of consumers want their bank to proactively recommend products and services (55% said it would increase their loyalty)

- 48% of consumers are interested in a spending analysis that is both real-time and provides a ‘forward view’

- 49% of consumers would bank with a company they currently use but that doesn’t offer banking services (77% of millennials, 58% of those 35-54, 28% of those 55+)

Millennial Acceptance of Branchless Banking

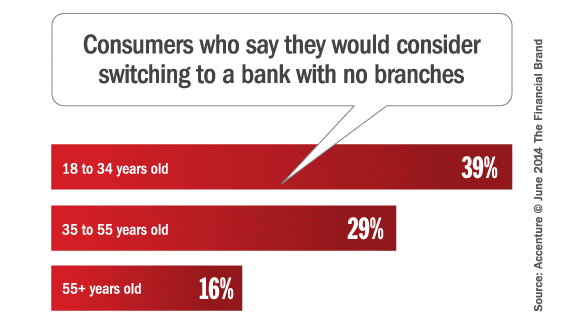

Consistent with several other recent studies, the Accenture survey found that younger financial institution consumers are nearly twice as likely as older consumers to consider switching to a branchless bank. The survey found that 39 percent of consumers 18 to 34 old would consider switching to a branchless bank, compared to 29 percent of customers 35 to 55 and 16 percent of customers over 55.

“For banks, simply being ‘more digital’ than what they are today will not be enough to assure success in the future.”

The acceptance of branchless banking across age categories illustrates how consumers are becoming less interested in convenient branch locations and more interested in accessing digital services at the time and place of their choosing. Another contributing factor could be that nearly three-quarters of US consumers considered their relationship ‘transactional’ rather than driven by advice or a broader relationship.

Millennial Acceptance of Non-Banks

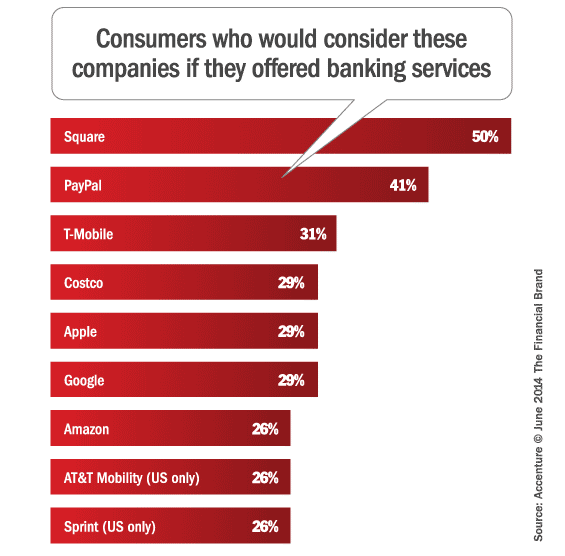

Beyond banking with organizations such as Square and PayPal that already offer forms of financial services, the Accenture survey found that significant percentages of younger consumers would be open to bank with technology and telecommunications players such as T-Mobile, Apple, Google, Amazon and even retailers if the companies offered the services.

“Banks that cling to the status quo risk being viewed over time more like utilities that conduct financial transactions.”

– Accenture

In total, 72 percent of consumers ages 18 to 34 would be ‘likely’ or ‘very likely’ to bank with at least one technology, telecommunications, retail or shipping/postal company they do business with if they offered banking services. More than half (55%) of consumers ages 35-54 and 27 percent of those ages 55 and older would be willing to do the same.

Among consumers aged 18 to 34, 40 percent said they would consider banking with Google, 37 percent with Amazon and 34 percent with Apple. Interestingly, for consumers ages 35 to 54, the numbers were still rather impressive, with 23 percent willing to bank with Google or Amazon and 20 percent with Apple. The numbers dropped significantly for those over 55.

Unlike previous surveys of this type, the Accenture survey shows the potential impact of T-Mobile as a threat to banks. Offering a prepaid checking account called Mobile Money, T-Mobile has 46.7 million customers, more than 70,000 branch offices, 42,000 fee-free ATMs, the same mobile platform that was used by Simple and a very impressive marketing budget. The power of this non-bank competitor could only increase if T-Mobile and Sprint merge.

“Tomorrow’s consumer is coming of age with a very different perception of what a bank could be,” said Wayne Bush, managing director of Accenture’s North American Banking practice. “Those expectations could be profoundly disruptive to banks if non-bank entrants gain momentum and banks fail to adapt quickly. This will have important implications for the ‘digital generation’ spanning nearly all age groups.”

Some of the larger banks have noticed the potential presented by non-bank players. “We are in a new era for Wells Fargo,” stated chief marketing officer Jamie Moldafsky at an industry conference. “Historically, when people have asked, ‘Who are your competitors?’, we would answer Chase or Bank of America. Today, we would answer Google or Amazon.”

Bank of America has responded by offering a checkless checking account designed to appeal to millennials. The account has a fixed $4.95 monthly fee and offers no paper checks. The idea is to build loyalty with younger customers by charging them lower fees and offering an account with online, mobile and card transactions only.

( Read More: 7 Reasons Mobile Money From T-Mobile Should Worry Bankers)

Millennials Want Proactive Advice

A potential bright spot for traditional banks is that, while millennials may no longer desire bricks-and-mortar branches to do their banking, they want their financial services provider to be more engaged in their life, offering insights into their spending and help with their major purchases such as a car or house.

According to the survey, younger customers were also more likely than older consumes to want their banks to proactively offer products and services to help them with money management.

-

- Respondents ages 18 to 34 would like their bank to help them buy a car (55%) or with purchasing a home (57%).

- 68 percent of younger responders expressed interest in receiving real-time analytics of their spending, including safe-to-spend forecasts, compared to 55 percent of those ages 35 to 55 and 24 percent of those over 55.

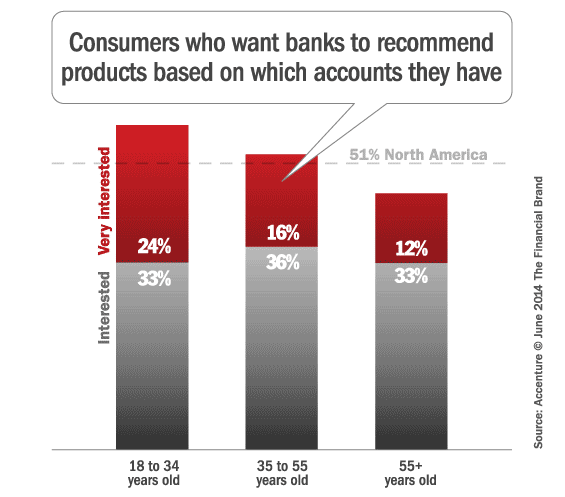

- 57 percent of millennials want their bank to recommend products or services that they might need, while considering which accounts they already have.

“Banking is widely viewed as simply a transactional activity, but people are seeking advice and relationships that improve their financial well-being,” said Robert Mulhall, a managing director in Accenture Distribution and Marketing Services. “In this digital era, the most successful companies focus on solutions rather than products to simplify their customers’ everyday lives. Banks need to think this way.”

“Digital technologies are dissolving the boundaries between industry sectors,” said Juan Pedro Moreno, senior managing director of Accenture’s Global Banking practice. “They will need to move beyond their traditional role of enablers of financial transactions and providers of financial products to play a deeper role in the lives of their customers – by applying digital technology in new ways and by offering tangible value and advice based on transaction information.”

Read More: How to Build an Everyday Bank

Recommendations

To address the challenges described, Accenture recommends banks launch an attack on three fronts:

- Seamlessly integrate across in-branch, assisted and digital interactions: Some consumers of all ages still value the branch, where nearly 60 percent of traditional retail bank products are still sold. But as more consumers use online, mobile and tablets for banking, there is a greater desire for a bank that is agile and innovative, with the digital tools to connect with them on a daily basis.

- Become a part of consumers’ daily lives: Similar to the strategy being implemented by Square, banks need to build a digital ecosystem with existing provider partners and other key players in areas such as home goods, health, travel and leisure, communication, and transportation. These partnerships would include presale advice, discounts, post-sale support, cross-sale opportunities, and more.

- Offer digital personalized advice and counseling: 74 percent feel their bank should provide tools to make their life easier. Automating the generally manual process of budgeting will satisfy a basic desire of customers.

In study after study it is clear that consumers are calling for a new service proposition – they want their bank to make their financial lives easier and to enable them to manage their money more proactively. They are looking for an agile partner that continues to innovate. They are also looking to do more and more of their banking on digital channels and would eventually like advice to be delivered through the same channels.

The question is whether traditional banks will meet the challenge in the near term or will be caught flat footed as a non-traditional provider introduces a value proposition desired by millennials and older digital consumers.