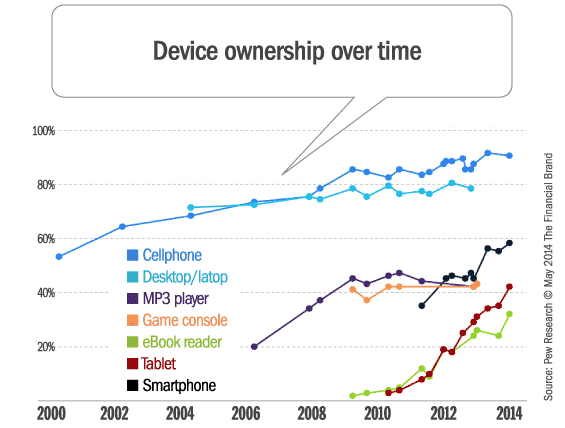

Ownership and usage by device type continues to change rapidly as more consumers are moving to smartphones and tablets for daily digital activities. As can be seen below, smartphone and tablet ownership is skyrocketing, while ownership of traditional cellphones and desktop/laptop devices are starting to decline.

Changes in usage by device type are also changing rapidly, with smartphone and tablet website visits each increasing by almost 50% over a one-year period. While still dwarfed by website visits made via desktop/laptop, the trends still illustrate the importance of mobile devices.

| Website Visits by Device |

Q4 2012 | Q1 2013 | Q2 2013 | Q3 2013 | Q4 2013 |

|---|---|---|---|---|---|

| Desktop/Laptop | 81.6% | 79.8% | 78.8% | 76.1% | 73.2% |

| Tablet | 9.6% | 11.2% | 12.0% | 13.2% | 14.6% |

| Smartphone | 8.8% | 9.0% | 9.3% | 10.7% | 12.2% |

| Tablet Visits by Device |

Q4 2012 | Q1 2013 | Q2 2013 | Q3 2013 | Q4 2013 |

|---|---|---|---|---|---|

| iPad | 91.1% | 90.6% | 90.5% | 88.9% | 87.5% |

| Kindle Fire | 2.7% | 1.9% | 1.5% | 1.4% | 2.0% |

| Android | 6.2% | 7.5% | 8.0% | 9.7% | 10.5% |

| Smartphone Visits by Device |

Q4 2012 | Q1 2013 | Q2 2013 | Q3 2013 | Q4 2013 |

|---|---|---|---|---|---|

| iPhone | 60.8% | 62.7% | 62.3% | 60.8% | 59.6% |

| Android | 38.3% | 36.2% | 36.5% | 37.9% | 39.0% |

| Windows | 0.9% | 1.1% | 1.2% | 1.3% | 1.4% |

A Multi-Screen World

According to a Google study, we have become a world of multi-screeners, with 90 percent of a consumers’ media interactions (4.4 hours a day) done on a computer, smartphone, tablet or TV. The device selected is often driven by context – where we are, what we are doing, what we want to accomplish and the amount of time we have available.

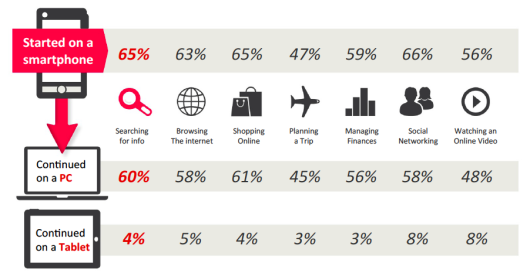

While some of our multi-screening is accomplished by moving between devices, we also use multiple devices simultaneously, with smartphones being the backbone of the majority of our daily interactions. Smartphones not only command the highest percentage of user interactions (38 percent), but also serve as the most common starting point for activities across multiple screens.

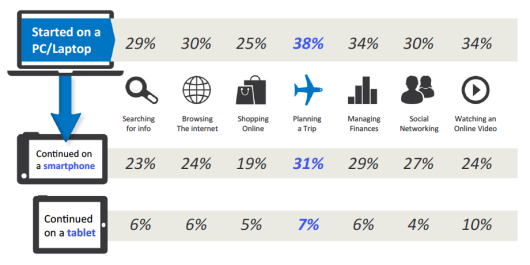

As shown below, 59 percent of multichannel financial interactions begin on a smartphone with 56 percent moving to a PC/laptop. Alternatively, 38 percent begin on a PC/laptop with 31 percent moving to a smartphone. For banks and credit unions, the goal should be to make these cross-channel interactions as seamless as possible and to simplify the overall customer experience.

Importance of Cross-Channel Integration

In the 2013 World Retail Banking report by Capgemini and Efma, there was a clear correlation between a positive customer experience and a consistent multi-channel experience.

- On average, customers with positive customer experiences in 85% of the cases said that their banks are doing a good job of offering consistent experiences across channels.

- Only 34% of customers with negative experiences said they think their banks provide consistent multi-channel experience.

The report also highlights that as products and services are turning into commodities, channels offer one of the greatest opportunities for banks to differentiate themselves.

“One thing we’re not trying to drive is the proliferation of more and more apps … customers don’t want that. We want to create that single platform that’s device agnostic.” – Simon Pomeroy, Westpac

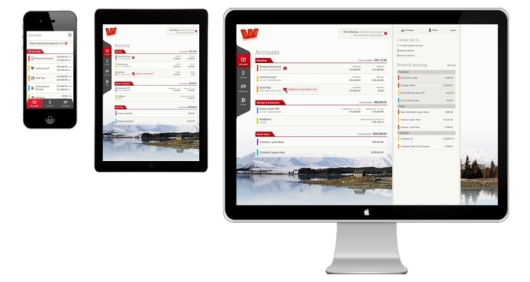

As branch transactions continue to decrease, and smartphone and tablet interactions with banks continue to escalate, the importance of an integrated and seamless multichannel experience increases. One way of moving towards that ‘ultimate experience’ is by implementing a device-agnostic strategy like seen with Westpac (NZ). Westpac invested $15 million in its new central platform, which aims to offer a full-featured banking experience across smartphones, tablets and PCs.

Some institutions are also providing digital tools such as tablets and interactive digital kiosks to login and execute self-service tasks and/or to engage with product guides in an interactive fashion.

Moving From Channels to Seamless Experiences

Multi-screen has become the new normal and banks and credit unions must adapt to this reality. The choice of device primarily comes down to the path of least effort to complete a given task. To illustrate the advances banks have made worldwide in cross-channel integration, Mapa Research utilized their portfolio of 50 live accounts across 10 countries. Worldwide trends and specific examples have been summarized in an excellent 78-page report entitled, ‘Winning the Key Strategic Banking Battles: Cross Channel Experiences.’

The key objectives of the research were to:

- Examine the experiences across digital banking channels – primarily focusing on desktop, mobile and tablet, but when relevant also include content around branch banking

- Understand to what extent experiences are aligned (look and feel, functionality and security)

- Highlight unique, innovative and different developments in the following areas:

- Customer Initiation

- Navigation, Look and Feel

- Security

- Self-Servicing

- Sales and Marketing

- Customer Support

Customer Initiation

The process of becoming a new customer should be straightforward and simple. Unfortunately, despite great advances in technology to enable opening an account online or with a mobile device, most banks still have way too many steps and require significant effort on the part of the new customer. In fact, most processes still require a new customer to come to a physical facility to complete the process.

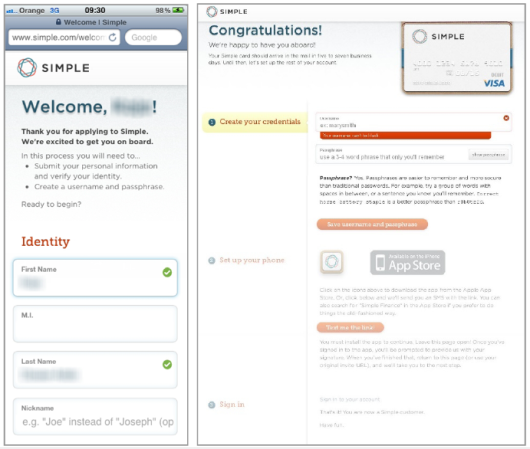

Mapa Research highlights the ease of opening a new account with Simple (recently acquired by BBVA). Simple allows visitors to become customers using an application that can be accessed from any type of device, hence providing freedom of choice. If approved, an email is sent confirming the new customer status. Login credentials (username and passphrase) are then established and the new customer signs an agreement using their smartphone screen.

Source: Mapa Research 2014

Read More: Easy Banking: The Simple Strategy

Navigation, Look and Feel

Mapa Research found that the majority of the desktop services reviewed now lag behind in terms of overall design and user experience. It was surmised that over the last couple of years mobile and tablet developments have been the priority. As mentioned, many banks are striving for a device agnostic experience similar to Westpac. Beyond an improved customer experience, development processes are streamlined.

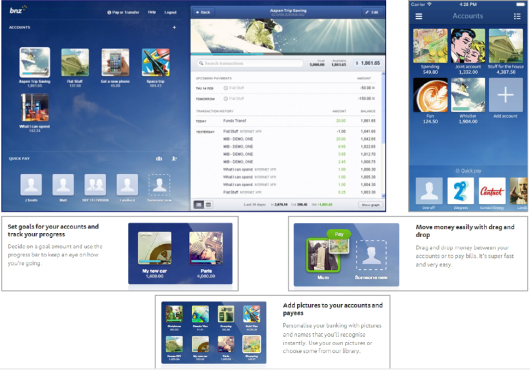

Some institutions were found to be developing platforms from a mobile-first perspective, applying many of the key mobile functionality, look and feel to the PC experience. While responsive design was found at several banks, implementation beyond login was still rare. The BNZ (NZ) example included in the Mapa Research report has similarity in design, look and feel including the iOS type icons – each representing an account.

Source: Mapa Research 2014

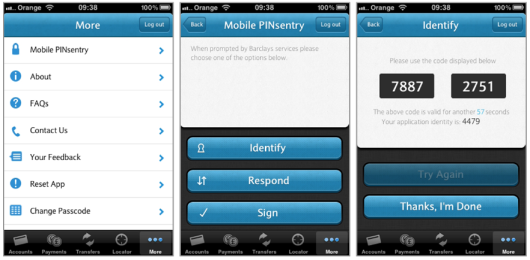

Security

Over the last 12 months, Mapa Research found that a number of banks have simplified their mobile login process by allowing customers to select a lower payment amount limit in return for lower security requirements. In some cases, the security options were the same for all channels, while other banks have different security methods by channel. Some even integrated security between channels such as providing security ‘tokens’ for online banking through the mobile device.

Source: Mapa Research 2014

Finally, a number of banks globally are beginning to test biometric security solutions, with several countries in Europe (Sweden, Denmark, Norway, Belgium) as well as New Zealand having country-wide initiatives to simplify the security process.

Self-Servicing

For better or worse, many organizations are adding access to more of a customer’s accounts via mobile devices according to Mapa Research. Additional functionality being added to mobile banking includes the ability to access more accounts, block cards, set alerts, transfer funds (both internally and externally), make payments and even manage investments or access PFM tools. The challenge is that this added insight and functionality can work against the goal of simplicity.

“On one hand this trend makes mobile banking apps feel more ’busy’ while it also means that users have yet fewer reasons to visit the desktop service,” stated Mapa Research in their report. Some institutions have addressed the challenge of scrolling by introducing a tiles-based approach providing shortcuts to key sections of interest. Others are using similar views regardless of device.

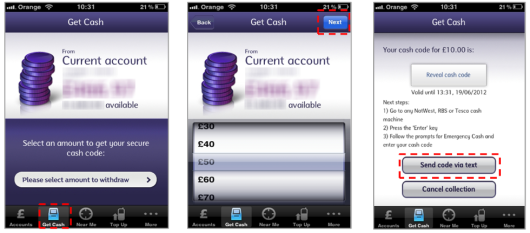

One of the more unique cross-channel integration examples is being done by RBS and NatWest in the UK, where a mobile device can replace a debit card to make withdrawals at an ATM. Access codes sent to a mobile device can even be forwarded to another person for P2P payments.

Source: Mapa Research 2014

Sales and Marketing

Despite the fact that more and more consumers are using their smartphones and tablets to shop and purchase financial services digitally, Mapa Research did not find very many examples of integrated sales and marketing communication by banks globally. There were several examples of banks that cross-sell services through the online banking app, but even then the completion (and sometimes initiation) of the process needs to be done at a physical facility. Mapa believes this is a significant area of opportunity for financial organizations.

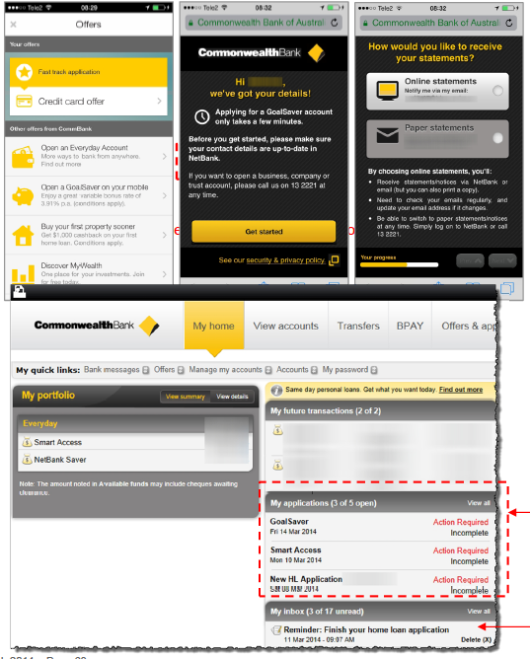

One of the few exceptions found by Mapa was with Commonwealth Bank in Australia, which has always been a leader in sales and service via mobile devices. One of the best features found was that a customer can begin an application process, leave the application and return later to finish the process either in the same channel or using a different channel.

Source: Mapa Research 2014

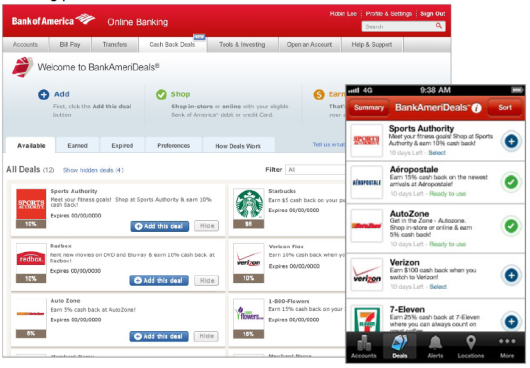

Another good example of cross-channel integration was found when an organization offered merchant-funded rewards through both the online and mobile applications. BankAmeriDeals has done an excellent job providing access to their Cardlytics rewards platform in an easy to navigate manner.

Source: Mapa Research, 2014

Customer Support

Mapa Research found that integrated customer support is getting better at many financial organizations, with secure messaging, live text chat, the ability to set branch appointments online all becoming available through mobile devices. Additional mobile support through augmented reality applications (for branch and ATM locations) is becoming increasingly available as is the ability to use mobile devices to copy and send important documents.

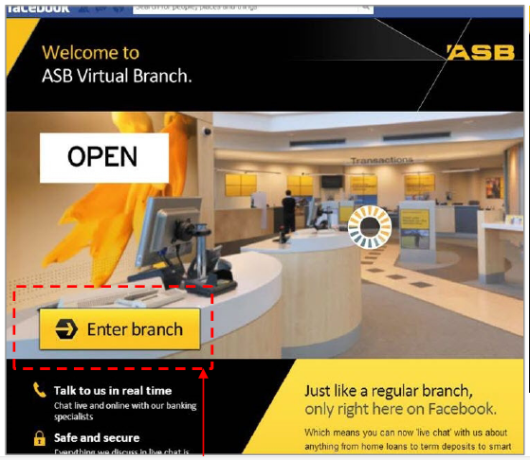

One of the most interesting examples of customer support across channels can be found at ASB Bank in New Zealand, where a ‘Virtual Branch’ is available for customers and non-customers on Facebook. Private and secure live chat can be requested expanding the bank’s reach beyond their physical footprint.

Source: Mapa Research, 2014

The Future of Cross-Channel Integration

While Mapa Research provides more than 50 examples of cross-channel integration being done at financial institutions globally, there are still many questions that need to be addressed from a customer experience perspective.

- Is the access to more accounts a better experience than easy access to fewer accounts?

- Is responsive design on multiple devices better than a unique experience based on the device being used?

- How do we focus on simplicity of delivery while dealing with the complexity of needs?

- How do we balance simplicity with security?

- Is the online channel becoming obsolete?

- How can we improve the sales process through mobile devices?

- Is there untapped potential with integrating payments, geolocation, social media and even branches?

- Is cross-channel or omnichannel a better customer experience solution?

Mapa Research Cross-Channel Experience Report

A 17-page introduction to the highly illustrative 78-page Mapa Research report on cross-channel experiences is available.