Specific marketing strategies for financial institutions looking to acquire new customers, improve product engagement, increase share of wallet, reduce attrition and enhance the customer experience. Some of the strategies are complex and are more difficult to implement, while others represent money that is left on the table if not initiated by a bank or credit union.

The key is to effectively prioritize your strategies and implement those that meet your organization’s goals while not burning unneeded resources.

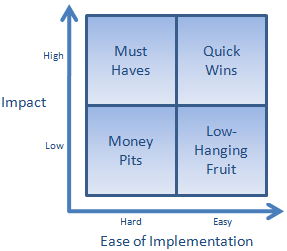

Strategy Prioritization Matrix

A Strategy Prioritization Matrix (SPM) is an easy to use tool to quickly and easily identify those initiatives from a wish list that offer the highest return for the least amount of effort. This tool is especially useful for organizations that have more marketing initiatives than can be funded, or where human resources are limited. The Strategy Prioritization Matrix quadrants include:

Quick Wins (High Impact, Low Effort) – These are the most attractive projects, giving you a good return for relatively low effort. Focus on these to build momentum and a strong ROI;

Quick Wins (High Impact, Low Effort) – These are the most attractive projects, giving you a good return for relatively low effort. Focus on these to build momentum and a strong ROI;- Must Haves (High Impact, High Effort) – While these provide strong returns, they take longer and use more resources, potentially crowding out viable ‘quick wins’. While these are important, they only bring a return when complete. Set deadlines for completion but don’t ignore their importance;

- Low Hanging Fruit (Low Impact, Low Effort) – While tempting, don’t focus too much on these unless they are creating a distraction to the accomplishment of either of the above. Do these in spare time, but put them to the side if a ‘quick win’ or ‘must have’ initiative comes along;

- Money Pits (Low Impact, High Effort) – These strategies should always be avoided. Not only do they provide low returns, but they crowd out time that is better used on any of the other three quadrants.

While the grid appears rather straightforward and simple, prioritizing initiatives is anything but simple since it requires the understanding of business priorities and the use of multiple evaluation criteria. Because each organization has different objectives and different dynamics around ease of implementation, the grid would not necessarily be the same for any two institutions.

By plotting your marketing strategies on the Strategy Prioritization Matrix, it will become apparent which initiatives need your focus. For most banks and credit unions, the first priority will be ‘quick wins’. If something is relatively easy to implement and it has the potential to have a large impact on your organization, do it, take the praise, build momentum, and move on to the next priority or quadrant.

While low hanging fruit may also be a good area to build momentum and impact a finite need, marketers can’t ignore the ‘must haves’ that provide the largest long-term impact.

Nothing is easy, but some strategies are both easier to implement as well as significantly impactful to a financial institution’s bottom line. Interestingly, many banks and credit unions are only doing one or two of these at this time. As a result, almost every financial institution can benefit from implementing more of the strategies below in 2013.

New Mover Customer Acquisition

There isn’t a business today that can exist without new customers. They are the lifeblood of any organization and the foundation for organic growth. Unfortunately, everyone is looking for new customers, so the competition for new customers is fierce and the cost of new customer acquisition continues to rise.

Although not as frequent as 4-5 years ago, people continue to move. And when people move, they make significant purchases for their new residence and make a conscious decision as to where they will shop, eat and bank going forward. These ‘consumers in transition’ represent both a risk for current providers as well as an opportunity for organizations wanting to acquire new customers (Bank Brand Loyalty Tested With Every Move).

For reaching these new movers, research found direct mail, email and word of mouth to be the most effective channels. Digital marketing has also increased in effectiveness as more movers use the web for research prior to and immediately following a move.

The keys to reaching this market in transition include:

- Be the first in the mailbox (or on the computer, phone, etc.) after a household moves to avoid other retailer and bank solicitation clutter and to benefit from early decisions

- Develop a system of immediate processing of prospects/customers to provide the foundation for being the first to reach the new mover

- Measure the incremental impact of the program against your alternative acquisition/retention efforts to prove the value of this strategy

A new mover program can be the foundation of their acquisition efforts, generating a ‘quick win’ that provides both a significant and consistent inflow of new customers. What is nice about this strategy is that once the process is established, little additional allocation of human resources is required.

Digital Retargeting To Support Online and Offline Marketing

While there are many forms of retargeting (see Banks Include Retargeting As Part of Digital Marketing Strategy), the concept of reaching out digitally to ‘double down’ communication messaging is gaining favor quickly as a means to improve results of both online and offline marketing efforts.

This strategy can include reaching out to people who visit your web page or who have started (and abandoned) a new account opening process, or could be a way to reach out digitally to people who are receiving a direct mail or email communication. Because of the ease and impact of this strategy, retargeting could be considered both a ‘quick win’ as well as a ‘must have’ initiative for banks and credit unions in 2013.

According to Lloyd Lee, senior vice president of integrated services for the direct and digital agency New Control, “The benefit of retargeting is clear – among all offline and online channels, retargeting is often the most efficient acquisition strategy on a cost per account basis.” Lee added, “For our clients, retargeting has become an ‘insurance policy’ since it ensures that we are capitalizing on all of the traffic we are driving to the client’s site from all of the online and offline acquisition efforts.”

As the technology and innovation in the digital space continues to improve, more opportunities are being explored with retargeting. For instance, one bank in 2012 achieved a lift in results of more than 40% when digital communication was targeted to households receiving a checking account acquisition direct mail package. Neither direct mail or online ads worked well independent of each other, but combined they achieved a very favorable CPA with only a modest amount of additional human or financial resource expended.

New Customer Welcome and Onboarding

Onboarding provides a unique opportunity for both a ‘quick win’ as well as a ‘must have’ strategy that sets the foundation for long-term customer relationship growth.

Despite the importance of this fundamental ‘must have’ strategy, there are still several institutions that have not taken advantage of the power of the ‘thank you’. 2013 should be the year that every institution either starts their onboarding process or enhances the process already in place.

For those organizations that do not have any program in place, it is time to commit to the ‘first touch’. This may be nothing more than a thank you letter with suggestions as to how to best utilize the account that has been opened. This letter of appreciation should not be just for new checking customers but also for new loan, credit card and small business customers as well. Outlining how to best use the account and discussing what other services align with the account opened will immediately reduce attrition, increase engagement and generate cross-sold accounts.

For those banks or credit unions that already have an onboarding program in place, the additional ‘quick win’ can be achieved by expanding your existing program to utilize additional channels such as digital retargeting (discussed above), email and even mobile communication. Some institutions have achieved an immediate WOW factor by sending a text or online offer from a local merchant to customers who opened a new account. Who wouldn’t want to receive a text informing them that they can pick up a cup of coffee or ice cream cone immediately after opening a new account in a branch or online?

Increasing Cross-Sales With Event Triggers

Today’s technology allows banks to identify event triggers more accurately than ever before. Beyond the traditional triggers such as balance increases and decreases and the renewal of a time deposit or opening or closing of an account, a customer’s digital footprint can provide insight into shopping behavior before a customer makes a decision.

‘Quick wins’ available with trigger marketing range from building a process of capturing a person’s email address or phone number when then call or shop for rates online to partnering with a credit bureau data provider who can tell you when your current customers are shopping for a credit product.

There’s power in using a tri-bureau data source to identify customers that may be shopping for a credit card, car loan, equity line of credit or mortgage. Knowing this information can serve to retain your current loan customers who may be looking to acquire new credit or refinance or could provide the foundation for a new loan solicitation.

Similar to all of the initiatives discussed above, setting up a trigger marketing program provides an annuity of revenues once the program is established with only limited human resources required on an ongoing basis. Despite the power of this type of communication, which takes advantage of right timed messaging, a surprisingly few organization have a disciplined approach to event trigger marketing.

Collecting Insights For Improved Communication

At a time when the term ‘big data’ is moving from buzzword to competitive weapon, it is time for banks to collect more insight from customers that can improve the relevance, timeliness, and effectiveness of communication. Yet many banks only have accurate email addresses on less than 50% of their base.

The results are further enhanced when we can personalize the message to the household decision maker (as opposed to the person who opened the account initially or the person listed first on the relationship file). And programs almost always exceed plan when we understand what products the customer has at other institutions, allowing us to only communicate with people in the position to switch existing relationships.

There is no reason for banks to try to perform analysis on unstructured social media ‘big data’ from their customers until they have effectively used data already on file within the firewalls or data that can be collected through rudimentary surveys and revised new account processes.

As discussed above, one of the best ways to accelerate marketing results (and potentially receive additional funding) is to orchestrate a number of relatively small ‘quick wins’. These wins not only give your team a reason to celebrate success, but also generates the energy and motivation needed to tackle larger, more ambitious initiatives.