In August, Richard Cordray, head of the CFPB, announced that the agency was turning its gaze toward student loans. So it was no surprise when, earlier this week, the CFPB’s student loans ombudsman Rohit Chopra posted an article on scoring student loan servicers to the agency’s website. It may have been a surprise to Sallie Mae, however, when he called the company “the worst in borrower, school, and federal personnel satisfaction.” Although the CFPB did not announce any monetary penalty, the findings will affect the company’s bottom line since it will be allotted “the fewest new loans to service in the upcoming school year.”

And those fines may still be coming. The company itself has warned investors that it “expects the Federal Deposit Insurance Corp. to publicly accuse it of violating several federal laws regarding its private student loans. The Department of Education has said that it, too, was probing the company to ensure borrowers with taxpayer-backed loans were not harmed.”

The most frustrating aspect of this for Sallie Mae must be the fact that this should not have been a surprise. In fact, it need not have happened at all. If the company had been monitoring its customer experience to identify emerging pain points before they escalated to the CFPB, it wouldn’t be in this situation and its customers would be much happier.

Over a month ago, Beyond the Arc posted an article on its blog warning Sallie Mae that their student loans practices would draw the CFPB and other regulators’ watchful eyes. Beyond the Arc regularly mines the CFPB’s consumer complaint database to help identify customer experience pain points so banks and credit unions can take action before the CFPB does. In Sallie Mae’s case, the data showed there was clearly a problem that needed to be addressed. Here’s a brief recap of the analysis.

Read More: 10 Things Every Financial Marketer Should Know About The Student Loan Crisis

A focus on student loans

Richard Cordray did not mince words when he announced the agency’s focus on student loans last month. “It’s a big priority for us,” he said, adding that borrowers “come to our complaint line and they come by the thousands.”

That’s no exaggeration. As of August 12, 2013, the public CFPB complaint database contained 4,427 student loan complaints about private lenders. According to a mid-year report on student loans recently released by the CFPB, outstanding student loan debt is approaching $1.2 trillion. At $165 billion, private student loan debt accounts for 14% of that total. The report goes on to cite the “disproportionate use (of private student loans) by high-debt borrowers. For borrowers graduating around the time of the financial crisis with over $40,000 in student debt, 81% used private loans.”

Cordray openly expressed interest in this subset of the population: “Frankly, those are the people we should care about as much as anyone in our society… They are young people with some amount of promise and talent and they just lack the means.”

Given the evident importance of private student loans to the CFPB, it’s important that financial institutions understand the complaint data the agency uses when making regulatory and investigative decisions.

Read More: Big Banks, Big Complaints: CFPB’s Database Reveals Trends

Let the data speak

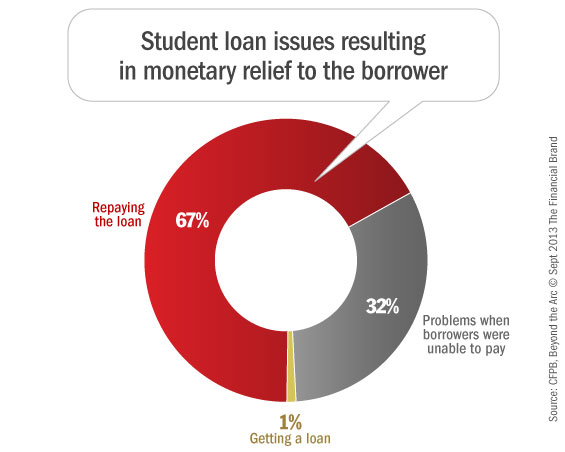

To determine which lenders should potentially be concerned, we took a look at which types of student loan complaints are currently resulting in monetary relief to the customer. Out of all 4,427 student loan complaints, 258 or 6%, resulted in monetary relief. As you’ll see in the chart below, the most prevalent issue resulting in monetary relief was “Repaying your loan.” This was the most frequent issue for student loans overall.

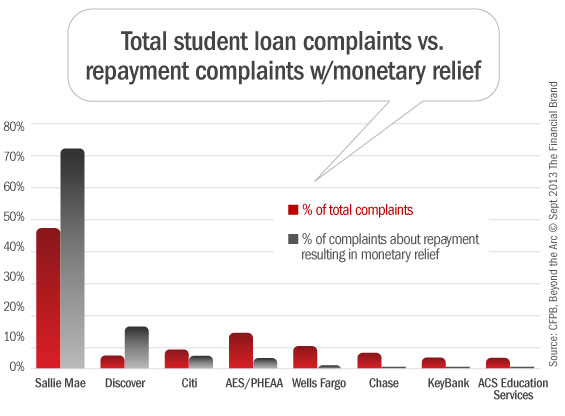

Next, we looked into which financial services companies had the most complaints about loan repayment that resulted in monetary relief. As you’ll see in the graph below, Sallie Mae generated the most activity, accounting for 46% of all student loan complaints (the blue bar). More importantly, it represented a disproportionate percentage of complaints about loan repayment that resulted in monetary relief (the red bar). 76% of these complaints were about Sallie Mae. This should have been a red flag to the company, as it mostly likely was to regulators at the CFPB.

Further examination revealed that Discover is also facing the same issue, albeit on a much smaller scale.

Read More: Wells Fargo Soft Sells Student Loans Through Social Media Forum

Be proactive not reactive to avoid regulatory risk

Our analysis indicated that Sallie Mae had an opportunity to improve their loan repayment process to avoid regulatory risk. As the company had access to specific complaints, they could have tried to determine the root cause of these complaints and fix the problems. They still have that opportunity, but their bottom line has already experienced a direct impact.

Other companies can learn from Sallie Mae’s example and take action well before customers lodge complaints with the CFPB. Banks and credit unions now have access to millions of customer feedback data points from multiple channels and sources. A typical bank captures not only customer profile and transactional data, but also customer emails, survey data, banker notes, escalations, and complaints. When you factor in publicly available data sources such as social media and the CFPB database, you begin to gain a very clear view of the customer experience.

The keys to avoiding the trap Sallie Mae fell into are analysis and action. Just capturing the data itself does not make it useful. You need to have established analytical and reporting processes in place in order to identify emerging pain points. Even more importantly, you must have business practices in place for taking swift and decisive action. The analytics team should be integrated with the lines of business to alert them so they can make changes. Then, the results of these changes need to be measured through continued monitoring so you can demonstrate success or improve the solution if necessary.

Brandon Purcell is the Data Science Team Lead at Beyond the Arc, a consulting firm that provides financial institutions with the strategic guidance and advanced analytics they need to grow their business.