2013 marks the third year The Financial Brand has fielded its annual “State of Marketing in Retail Banking” study.

In a previous article, The Financial Brand presented an analysis of the marketing landscape in retail banking, revealing marketers’ strategies, priorities and challenges in 2013. This view into the survey will identify the financial institutions who outperformed the pack, and uncover the marketing practices that distinguish them from other financial institutions.

High-Performing Financial Institutions

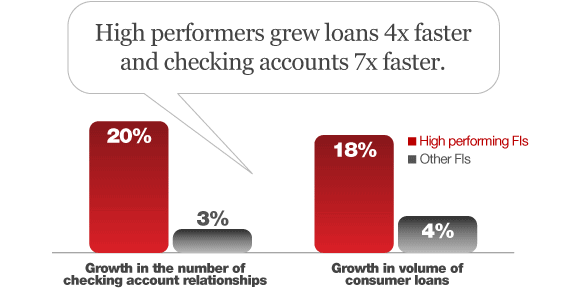

We characterized a bank or credit union as “high-performing” if it grew its checking account customer base and the number of retail loans it issued in 2012 by more than 10%. Using this criteria, 12% of survey respondents qualified as a high-performing financial institution.

High-performing financial institutions averaged 20% growth in checking account relationships in 2012, and enjoyed an 18% increase in the number of consumer loans issued. In contrast, among other financial institutions, checking account growth averaged just 3%, and consumer loans grew just 4%.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

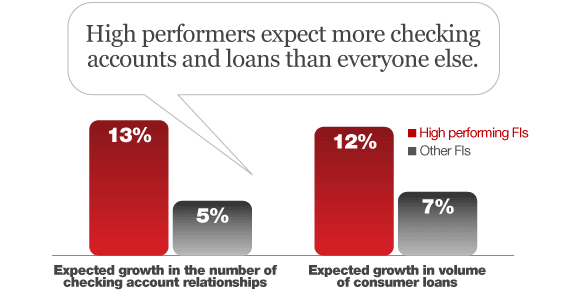

If all goes to plan in 2013, the high-performers will repeat last year’s performance. On average, high-performing financial institutions expect checking account relationships to grow 13% in 2013, more than double the expected growth rate of other financial institutions. In addition, the high-performers are anticipating 12% growth in loans, in contrast to the 7% growth rate that other banks and credit unions expect.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

Marketing Hallmarks of High-Performers

What distinguishes the high-performers from other financial institutions? Our analysis identified five practices that high-performers do—or tend to do—that other financial institutions don’t, including: 1) How they build and nurture their brand; 2) Which products they’ll focus on marketing; 3) Their marketing analytics capability; 4) What they’ll do with branches; and 5) What they measure.

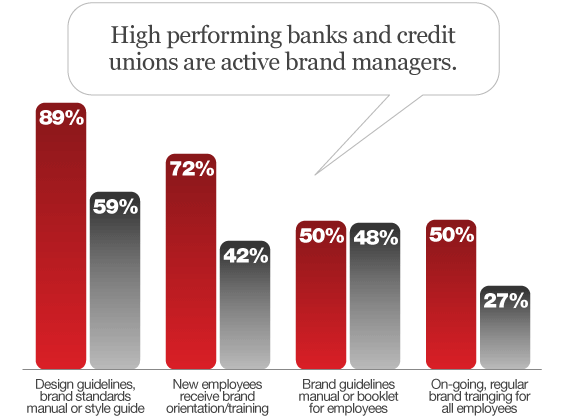

#1) High-Performers Build and Nurture Their Brand

While 6 in 10 average financial institutions have a brand book of some sort, nearly all high-performers have a manual or style guide describing the organization’s brand standards and design guidelines. But it’s not enough to have a manual; it’s what you do with it. Most high-performers provide brand orientation or training to new employees. And about twice as many high-performing financial institutions deliver on-going brand training to all employees as other financial institutions do.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

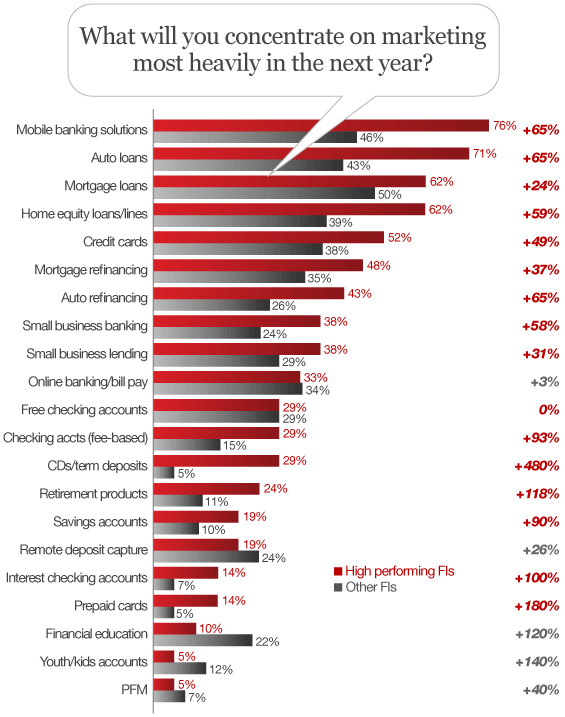

#2) High-Performers Will Focus on Lending Products

Three-quarters of high-performing financial institutions will concentrate on marketing mobile banking solutions in the next 12 to 24 months, in contrast to about half of all others. In addition, a larger percentage of high-performers will focus on a range of loans (including mortgages, auto, credit card, and refinancing) than other financial institutions will.

Although deposit products aren’t as big a focus area for anyone this year, a larger percentage of high-performers will be focusing on fee-based checking accounts, certificates of deposit, and savings accounts. This is consistent with their higher growth projections for checking account relationship growth in 2013.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

#3) High-Performers Invest in Marketing Analytics

Today, a little more than half of high-performing financial institutions use analytical models (e.g., next best product, attrition, response, media mix, etc.) for credit and deposit products, compared to 4 in 10 other financial institutions.

But that gap will widen throughout 2013, with almost 30% of high-performing financial institutions developing or enhancing at least four different marketing analytical models for credit products. One in three high performers will develop or enhance four or more separate models for deposit products. Just 10% of other financial institutions will keep up with this development/enhancement pace.

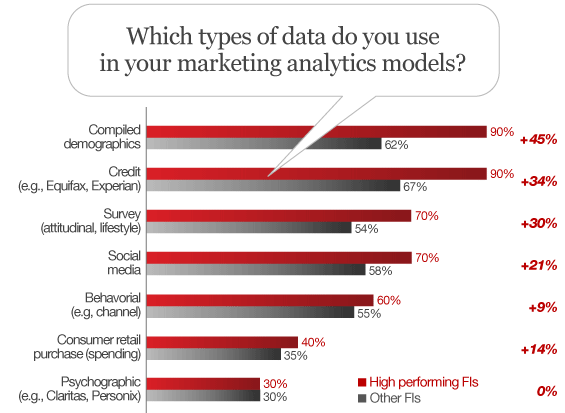

High-performers also use different types — and a wider variety — of data in their marketing models. Nearly all use compiled demographics and credit data, in contrast to about two-thirds of other financial institutions.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

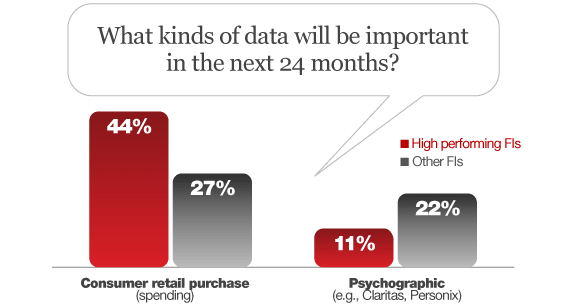

Looking ahead, the differences in the types of data used in analytics efforts will change, as well. 44% of high-performers will place a greater emphasis on using consumer spending data, in contrast to just a quarter of other financial institutions. Twice as many other financial institutions as high-performers, however, consider psychographic data to be important over the next couple of years.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

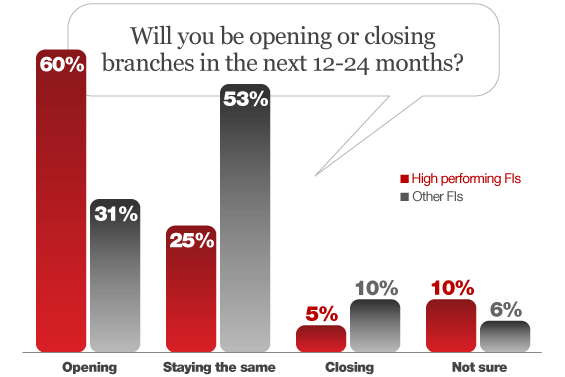

#4) High-Performers Continue to Invest in Branches

In the press and around the blogosphere, the debate about the death of bank branches rages on… but not in the offices of high-performing financial institutions. 66% of high-performers plan to open more bank branches throughout 2013 stretching into 2014, twice the percentage of other banks and credit unions that plan to do so.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

A previous study conducted by Momentum in conjunction with The Financial Brand found credit unions that added branches vastly outperformed those that didn’t, and along every measure — asset growth, member growth, loan growth and ROA.

#5) High-Performers Look Outward

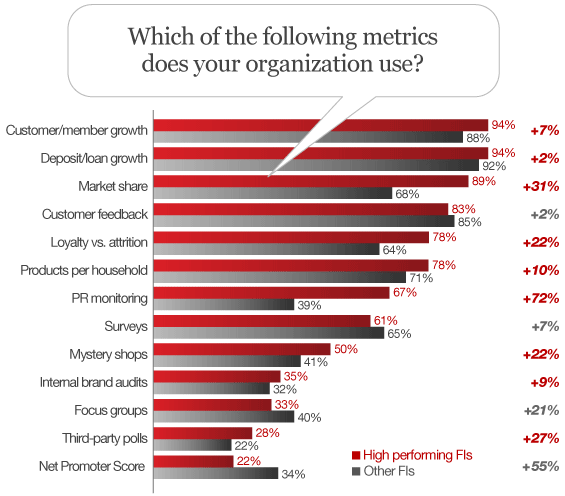

An overwhelming majority of all financial institutions use growth of customers (or members), deposits and loans as metrics to evaluate their marketing performance.

Across many of the other metrics, little difference between high-performers and other financial institutions was observed. We did, however, find differences in three key areas. The first was in the evaluation of market share, which nearly 9 in 10 high-performing financial institutions look at vs. 68% of other banks and credit unions. Second, high performers are actively monitoring and measuring the volume of PR they receive.

What’s significant about these two metrics (market share and PR monitoring) is that they are externally — not internally — focused. These metrics require financial institutions to look outside their four walls, which, in turn, requires an investment of capital resources. A larger percentage of high-performing banks and credit unions are willing to make this investment.

The third difference observed was in the use of Net Promoter Score. For all the press and hype this metric receives as being the “ultimate” question, just 22% of high-performers calculate their NPS, in contrast to a third of other financial institutions.

Source: The Financial Brand/Aite Group survey of 258 financial services executives (2/13).

Becoming a High-Performer

High-performing financial institutions execute their marketing efforts differently than other financial institutions do—that’s what this research shows. We’re not deceiving ourselves (nor trying to deceive you, the reader) that an financial institution can just measure a few different things, invest in branches and analytics, and focus on branding and lending in order to become a high-performer.

But what we do think this research shows is that high-performers have their marketing act together across a range of activities—and not just one or two. Just 12% of survey respondents qualified as a high-performer by our criteria. The bar is set high.